Washington’s Initiative 1098 has sparked debate about the impact of income taxes on small business. (See opinion pieces here, here, and here, for example.) There seems to be some confusion—as well as some claims on the outer edge of truthfulness—so I’ve put together a triplet of charts that may help clarify things.

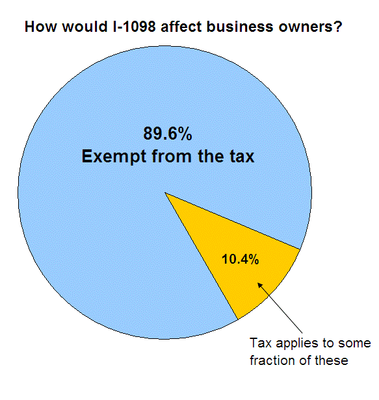

First up, here’s a look at how business owners would fare under 1098:

The data used in this chart come from research by the Economic Opportunity Institute.

What the numbers show is that only one-tenth of all “Washington tax filers claiming net business income from a sole proprietorship, S-corporation and/or partnership” report more than $200,000 in income, the threshold for I-1098’s tax on single filers.

In fact, these numbers actually overstate the reach of the tax in at least two ways. First, there are actually more business owners than shown (those with losses) who are exempt from the tax, thereby shrinking the real percentage of total business owners who are subject to it. Second, and more importantly, a significant share of the business owners are actually joint filers, which means that they would be exempt from the tax provided that their annual household incomes are below $400,000. As a result, it’s fair to say that fewer—probably much fewer—than one-tenth of all business owners would pay any state income tax at all under 1098.

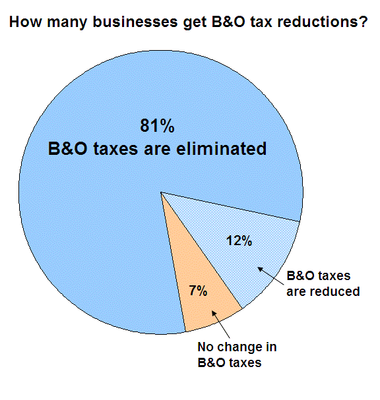

Next, let’s look at how many businesses would get tax cuts. This one’s a two-parter.

Here’s the picture for the state’s Business and Occupation tax:

Data come from reporting in the Vancouver Columbian as well as research by Economic Opportunity Institute. (Both sources say that the numbers come from Washington’s Department of Revenue.)

All told, the B&O tax reductions will mean that businesses in Washington will pocket an extra $250 million a year starting in 2012. And because of the way they are structured, the B&O tax cuts will be most beneficial to smaller businesses. The roughly seven percent of businesses that won’t get a reduction are the state’s biggest businesses.

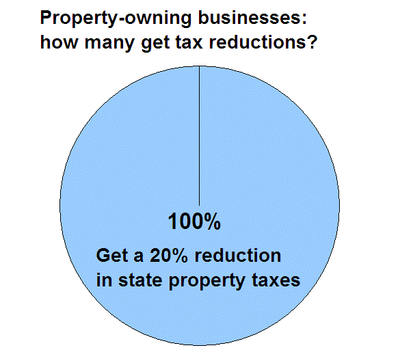

Finally, here’s a (partial) picture of state property taxes:

This chart is a little obvious I suppose, but the point tends to get overlooked: 1098 will provide an across-the-board 20 percent cut in state property taxes for all property owners, including individuals, businesses, and anyone else who pays property taxes. It’s true, as some folks like to nitpick, that local property taxes are higher than state property taxes. But that oft-repeated claim doesn’t change the underlying math: 1098 reduces state property taxes by 20 percent. (More detailed property tax savings are available from Economic Opportunity Institute.)

There’s a clear benefit to property owners, but also a benefit to renters and lessors because landlords tend to pass along the cost of property taxes to their tenants. So it is reasonable to expect that even businesses (and individuals) who lease or rent property will benefit indirectly from a lower state property tax burden.

Needless to say, these charts can’t illuminate how any particular business would fare under 1098. But I think they strongly suggest that small businesses—and small business owners—will actually benefit from 1098. Now it’s perfectly possible, I suppose, that some small fraction of business owners will find themselves at a net tax disadvantage under 1098, but I think for the moment, the burden of proof is on the opposition.

jjjpl

Doesn’t that same EOI report say that the 10% of businesses is really 5% of sole proprietors (who don’t hire anyone) and 28% of S-corps & partnerships? I get it that most home-based businesses won’t pay the tax, but 28% of job creating businesses is a lot. Actually, taxing 10% of businesses is a lot when you’re talking about jobs. The income tax will gross $3B. that’s also a lot.For the B cut, how many businesses are already exempt? Proponents are taking credit for 80%, but I’m pretty sure that most of those already don’t pay.And the OFM report shows the average B cut to be $1,600. I’d love to get that check (it’s bigger than the checks President Bush sent out), but it won’t do anything to grow the business.

Eric de Place

Readers can find the EOI memo here: http://www.eoionline.org/tax_reform/fact_sheets/SmallBusinessIncomeTax-Jun2010.pdfJJJPL—Your EOI figures are accurate w/r/t to sole proprieterships and partnerships/S-corps, but I might quibble with your interpretation. Sole proprieterships actually represent jobs and real income for households. And while it might seem like 27.7% of S-corps/partnerships might be on the hook for some income tax burden, the real figure is likely lower, and perhaps drastically lower. That’s because a share of those are joint filers who would fall below the $400k threshold. In fact, the average income of S-corps is less than $318k! Plus, keep in mind that we’re not actually talking about taxes on businesses per se—we’re talking about taxes on business owners. Those are different creatures, and it’s not at all clear (at least to me) that there’s any jobs-related harm in levying a modest tax on business owners who are reporting significant business income. Particularly not when there are offsetting tax reductions in the B and O and state property taxes.Finally, I don’t see the $1,600 figure you reference from OFM’s report. If you have it, please send it to me!

jjjpl

http://ofm.wa.gov/initiatives/2010/1098.pdfIt's the $250M / 157,000 small businesses benefiting from the B cut.the report also shows the average income tax bill would be $76,000 after it ramps up in 2013. We’re talking about pulling $3B out of the private sector in huge chunks while spreading $250M worth of small checks to other businesses (nearly no one earning over $200K will get the B cut). The 4% property tax cut, IMHO, is not really a sound policy decision but a sweetner to win votes.The reason 1098 hits business decisions is because it taxes S-corp and Partnership income even if it’s left in the business for reinvestment. Most successful businesses reinvest a significant percentage every year. Go talk to some businesses that employ 20-500 people and ask them what they think about paying a marginal 9% for every $1 million they reinvest. These folks drive our economy.

Eric de Place

Thanks for the OFM clarification, JJJPL.But I’m not sure you’re giving a fair depiction of the policy now. According to OFM, in 2013, $633 million gets plugged right back into the private sector in the form of B and O and property tax reductions. On net, we’re talking about less than $2.3 billion in new revenue for the state. But what I really don’t get is this: even for folks pulling in $1 million a year as a single earner, 1098 would make Washington entirely unexceptional with respect to income taxes. We’d be drastically lower than California and Oregon, and a meaningful amount lower than Idaho, Montana, New York, New Jersey, Minneosta, Wisconsin, North Carolina, South Carolina, etc. In fact, our effective income tax rate at that level would be just about exactly like Georgia, Virginia, Connecticut, Missouri, and Ohio. So what I am missing? Are all those states considered hostile to (small) business?

Francis

It’s about time Washington State tackled the B tax—it’s a textbook example of a market entry barrier, discouraging entrepreneurship. Basically, the current state tax code is a corporate welfare racket. I’ll do what I can to support Initiative 1098.

jjjpl

Eric-If you are honestly interested in understanding the business issues, I’m happy to oblige. Though I am serious in suggesting you find a business owner subject to 1098 and have them walk you through it.The issue is not the effective rate, it’s the marginal rate. That’s how business decisions are made.Say you own a manufacturing firm and are growing like crazy. You pay yourself an awesome salary, own some rental property, have a stock portfolio, etc and all of that combines to give you $1 million of take home. But your business shows an additional $1 million of profit that you decide to reinvest to install green technology next year.If you’re married, at $2M, your effective 1098 total tax rate is 6% (~the average OFM shows). Some owners look at that and say “I owe the state 6% of the money I leave in the business,” but more sophisticated owners understand that you have to think of the marginal rate of 9% (eg, what happens if you get a big order at the end of the year that doubles your profit…is that 6% or 9% tax rate? It’s 9%)More important than the effictive vs. marginal rate issue is the massive shock to the system of going overnight from 0% to 6% effective /9% top rate for profits that remain in the business. Other states simply haven’t had jumps like this. And yes, relative our existing lack of income tax, those other states are considered hostile.Compound that with 1098’s use of AGI, which takes the top capital gains rate to 24% this year and 33%+ in 2013. Capital gains rates drive your cost of capital when you search for investors.Personally, I’m not against paying more taxes if something makes sense. It’s just that 1098 doesn’t make sense to me when I look past the spin.Taking a giant step back, your pie charts imply that the state can give almost everybody a meaningful tax break, hit a few people with a trivial increase, and raise $2.5B in the process. That sounds like a magic formula that every state should have been using for the past 50 years. What’s the catch? “You can’t get something for nothing.”Those tiny wedges in your pie charts hire a lot of people and deploy a lot of capital. If we want WA to be a hub for green technology and biotech, we need to seriously understand the implications of 1098 on all kinds of businesses. Serious understanding means putting ideology on hold while you pursue honest answers from unbiased sources.I sincerely hope you have the time to dig fairly into all sides of this. 1098 is a huge deal for our state.

Kirk Richards

Far from being corporate welfare, the B tax actually reflects fairly the business done in the state, as opposed to the more usual profit tax, which subsidizes unprofitable businesses at the expense of everyone else.Looking at the pie chart, it’s incorrect to interpret that as the percentages of businesses affected by the proposed $3B tax. That’s the percentage affected in a given year. Many businesses have variable incomes, so if a big order comes in one year that pays for the next five years, the state will take a 9% bite out of most of that income.

Iona House

Eric–Interesting points. As with previous articles, you’re doing a nice job of presenting some pro-1098 points. But the graphs may be missing some key economic issues.For example, the big issue for business is not what percent of businesses get hit, but what percent of jobs get hit. 90% of businesses may be exempt, but that doesn’t translate into 90% of jobs (the smallest 90% of businesses supply only about 20% of the jobs). Making the claim that most businesses aren’t hurt is fine, but the more important economic question is the impact on jobs. Maybe you could show the graphs for business impact by total employees (or revenue, which may be a good proxy for jobs). Those graphs might tell a different story.

Eric de Place

Iona–If you have the data that jobs data, I’d be happy to crunch around in it. JJJPL–I understand the point about marginal cost, but I still don’t see an obvious connection to jobs impacts. As I understand things, when a business (or owners/shareholders) takes its profits and spends them on wages, that’s a business expense: it doesn’t count as income and it’s therefore not taxable under 1098. (Same would go for capital investments and the like.) In other words, business owners that spend money on employment are avoiding the tax, right?What IS taxed, is income awarded by the owner (even if that income is automatically reinvested in the business, unless it’s spent on business expenses, in which case it’s not). So I’m having a hard time seeing how taxing income from business owners who are pulling down $400k/year (assuming joint filing) is hurting jobs. Feel free to elaborate, folks. I’d like to develop a more sophisticated understanding of this!Kirk –I’m not sure you’ve characterized things accurately. The way I understand things, businesses can carry loses forward or backward in time. They can use a loss in the present year to get a refund on income tax they paid in a past year; or they can carry forward a loss in the present year to reduce tax liability in some future profitable year.

Iona House

Eric–Absolutely—the jobs data is here: http://www.census.gov/epcd/susb/latest/wa/wa–.htm The page has both the number of businesses and also the employees per business. Saw this site in the recent AWB survey, in which small employers suggested that they might cut back if the proposal passes. The survey release is here – http://www.awb.org/articles/pressreleases2010/survey_initiative_1098_would_hurt_small_business_job_growth.htm

JJJPL

Eric-It’s a question of timing.Reinvestment and hiring take time, budgeting and planning. 1098 throws a 9% marginal wrench in that.Think about a solid business that has an exceptional year. At the end of the year the owner looks at the books and decides he can open another location. First he must pay the 1098 tax. With what’s left, he starts construction. Then he buys the equipment (which is depreciated over time, not expensed). Then he hires the people. Then he opens and starts earning more income. Then he looks at the books to consider his next expansion.Lather, rinse, repeat.This is a simplification because owners are constantly evaluating new investments. But the IRS and 1098 take a snapshot at the end of the year to determine “profit.” At that point, any income – including income set aside for future reinvestment – is subject to tax at the owner’s marginal rate.At that moment, every year, the amount available to reinvest and hire is reduced.Compounding this is estimated taxes. 1098 makes business owners pay quarterly estimates of the tax due (kind of like paycheck withholding). So you have to pay before you even know your profit.As to your comment to Kirk-Kirk is correct. If someone earns $5M one year and loses money the next 5 years, they pay 1098 tax on the $5M, and get no refund for the future years. In fact they don’t even have to file with the state.The IRS has some strict “carry-back provisions” wrt petitioning for refunds of past payments due to current businesses losses, but 1098 has no such accomodation.

Iona House

Eric– Reposted with links instead of text – please delete the previous post. You’ll find the jobs data here The page has both the number of businesses and also the employees per business. Saw this site in the recent AWB survey, in which small employers suggested that they might cut back if the proposal passes. The survey release is here.Look forward to hearing your thoughts. Thanks.

Iona House

Eric– Take 3 – reposted with links – please delete previous posts. You’ll find the jobs data here The page has both the number of businesses and also the employees per business. Saw this site in the recent AWB survey, in which small employers suggested that they might cut back if the proposal passes. The survey release is here.Look forward to hearing your thoughts. Thanks.