")

")

In previous articles on Seattle’s proposed Mandatory Housing Affordability (MHA) program, I explained the program’s theory and risks, gave a broad critique of the math, and presented a case study of MHA for two types of mid-rise buildings, finding that MHA as currently drafted would suppress homebuilding and jeopardize the city’s affordability goals. Today: MHA’s high-rise upzones.

Seattle plans soon to launch MHA in the University District (U District), where the proposal includes upzones from mid-rise heights (65 to 85 feet) to high-rise (240 to 320 feet). You might think that tripling or quadrupling building heights would justify relatively high MHA requirements.

But applying the same kind of feasibility analysis I explained last time tells a different story. In large part because high-rise construction is so expensive, with today’s typical rents in the U District, new high-rise apartments conforming to the city’s draft MHA proposal would yield zero return on investment. In other words, adopting MHA as currently drafted for the U District would mean that for the foreseeable future it’s unlikely that anyone will build high-rise housing, denying the neighborhood much needed new homes—both market rate and subsidized.

To be fair, even without MHA requirements, high-rise apartments are typically not feasible in the U District today, and won’t be unless rents in the neighborhood escalate over time sufficiently to offset the big price tag of high-rise construction. The catch is this: the greater the net costs imposed by MHA, the higher the rents necessary for projects to pencil, and the longer homebuilding will be delayed. And during this waiting game of worsening scarcity, competition for what’s available, and rising rents, more low-income families and individuals will be displaced from Seattle.

Erring on the moderate side is the lower-risk path to keeping home prices down for everybody, citywide.

If passed as proposed, the U District high-rise MHA upzones will not only backfire on affordability by stalling high-rise homebuilding in the U District; they will also hinder the city’s progress on concentrating new homes around the U District’s future light rail station, and thwart equitable access to the neighborhood’s rich employment and educational opportunities. Furthermore, if the city sets the wrong precedent in the U District, it will likely “lock in” the same affordability-defeating MHA requirements for other neighborhoods, such as Northgate, where high-rise construction is at best marginally feasible today.

City policymakers have it within their power to avoid that lose-lose outcome for Seattle neighborhoods and local families: they can dial back the mandates. Fortunately, erring on the moderate side is the lower-risk path to keeping home prices down for everybody, citywide.

Where the U District numbers now stand

Because the U District is one of Seattle’s six designated Urban Centers and the site of a future Sound Transit Link light rail station, the city has been working to upzone the neighborhood since 2011. One of the plan’s primary objectives is to enable high-rise construction and “put more homes and jobs in the area directly served by light rail.” In the eleventh hour of the rezone process, planners integrated the city’s 2015 proposal for the new MHA program. Planners estimate that MHA in the U District will produce between 610 and 920 homes subsidized for lower-income affordability over the next 20 years. A final City Council vote on the U District rezone may come as soon as mid-February.

Under the original MHA proposal, all housing development in the U District would have been required to offer either 6 percent of homes at below-market-rate rent or pay a “fee in lieu” of $13.25 per square foot of building floor space. In Fall 2016, planners raised the requirements for the U District’s high-rise upzones to 9 percent inclusion and $20 per square foot (details here). The Seattle City Council is currently considering an amendment that would push the mandates even higher, to 10 percent and $22.25.

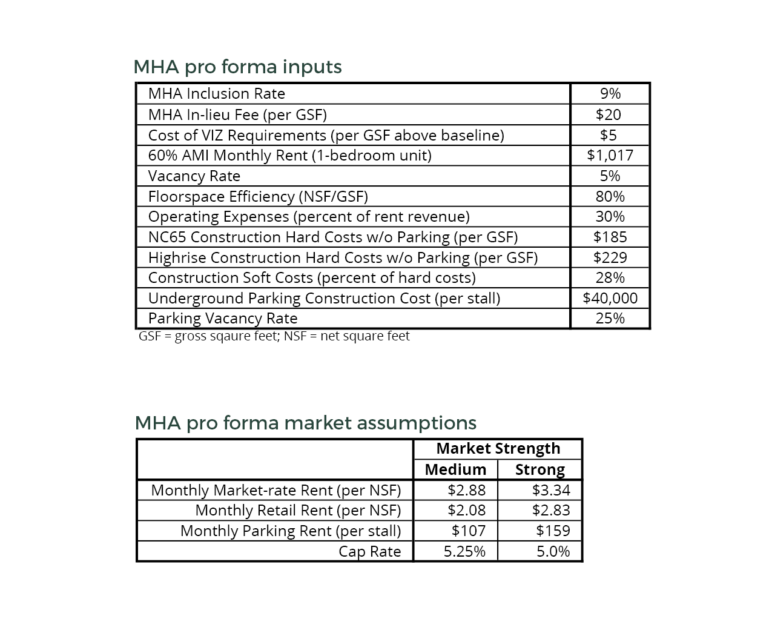

High-rise housing construction under the proposed U District rezone is also subject to the city’s Voluntary Incentive Zoning (VIZ) program that requires developers to build or fund amenities such as open space and historic preservation. Good ideas but these also factor into the cost of the project and must be part of the calculation (the city’s MHA feasibility study did not account for VIZ’s costs). Because builders can choose different VIZ options, the cost of meeting the requirements can also vary. For this analysis, I assume a cost of $5 per square foot of building capacity that exceeds the U District’s baseline floor-area-ratio (FAR) of 4.75 (see appendix for details).

Case study: NC65 to SM-UD240

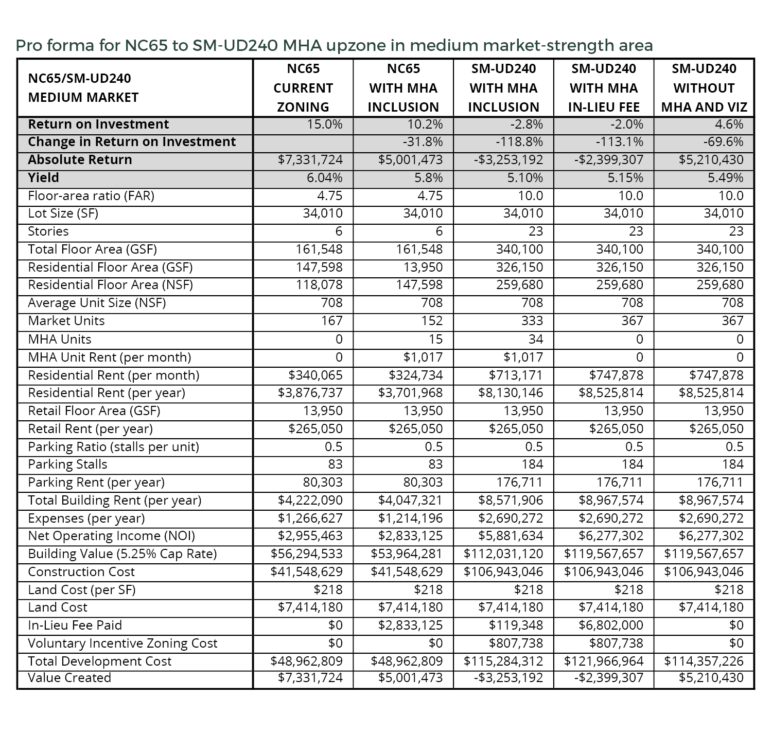

Following the before-and-after method I used previously, I applied simple, static pro formas—the standard process for real estate feasibility assessment—to analyze the proposed MHA upzone from the existing NC65 designation (“Neighborhood Commercial” up to 65 feet) to SM-UD240 (“Seattle Mixed – U District” up to 240 feet). Pro forma input assumptions and SM-UD240 building parameters are from the city’s MHA feasibility study. I adjusted land price to yield a baseline return on investment of 15 percent for a six-story mixed-use building that conforms to existing NC65 zoning. I then applied the same land price, parking ratio, and other inputs to a high-rise apartment building conforming to the MHA upzone.

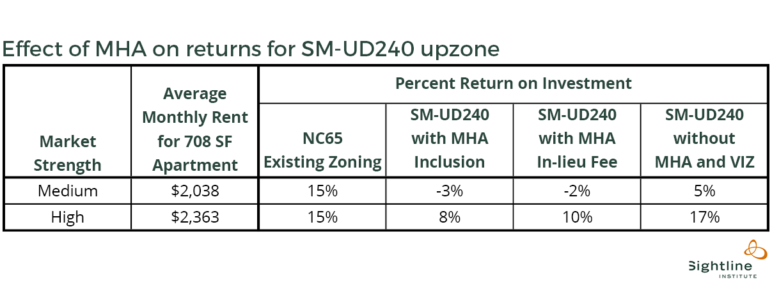

Pro forma results for percent return on investment are summarized in the table above. Under the city’s assumed existing medium market-strength conditions for the U District, compared to the baseline NC65 building, return on investment is totally wiped out for an SM-UD240 high-rise that meets MHA requirements. As shown in the far right column of the table, even without the added cost of of the MHA requirements, return on investment for the 240-foot high-rise is just 5 percent, a return that would not convince any investor to risk his or her millions of dollars.

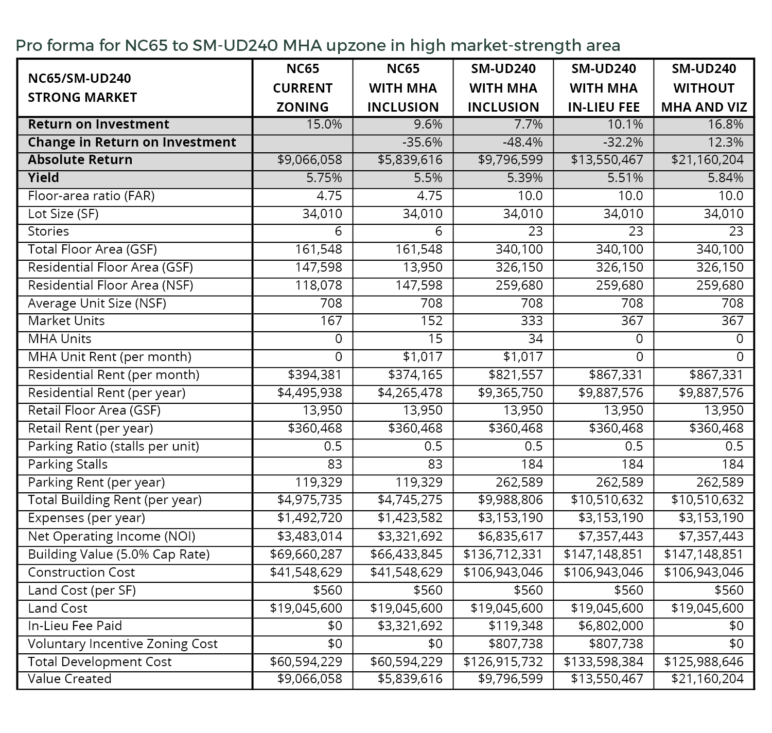

What if the U District’s average rents got higher at some point in the future? The bottom row of the table shows the return on investment under the city’s assumptions for rents in a high market-strength area. Compared to the medium market-strength case, in the higher rent scenario, the baseline NC65 building can support a land price about 2.5 times higher (see pro forma tables in the appendix). And in this scenario, MHA causes much less damage to return on investment for an SM-UD240 high-rise, demonstrating how higher rents can absorb more of the costs imposed by the MHA mandates.

Though improved by the higher rents, the high-rise returns are still much lower than the 15 percent yielded by the baseline NC65 building: the MHA upzone reduces returns by 48 percent and 32 percent for the inclusion and in-lieu fee cases, respectively. Both cases would be marginally feasible, if that. In contrast, without MHA, the 17 percent return exceeds the baseline case and falls well within the feasibility range.

The pro forma results show that under current conditions, the proposed MHA upzone from NC65 to SM-UD240 is not really an upzone at all, in practice. The value gained through the additional building capacity doesn’t come close to balancing the added expenses of the MHA affordability mandate, the greater cost of high-rise construction, and the VIZ charges. Surprisingly, even though the upzone grants a 111 percent increase in building capacity, the extra rent the larger building would yield isn’t nearly enough to make up for all the added costs. It’s hard to imagine how such a valueless upzone could meet the state’s legal standard for an “incentive” in conjunction with affordability mandates.

A 100-year lost opportunity for affordability

If implemented as proposed, the SM-UD240 upzone will result in fewer new homes built than if the zoning were left unchanged as NC65. Without MHA, a 240-foot high-rise in the U District would be extremely difficult to make pencil in the first place. MHA as drafted would drive the infeasibility nail deep into the high-rise coffin. The proposed SM-UD320 upzone is likely to exhibit similarly dismal feasibility performance, especially since it crosses the 240-foot threshold that triggers costly and time-consuming structural peer review.

In the near term, any housing built in the SM-UD240 zone would almost certainly be six-story mid-rise construction, like the baseline NC65 building analyzed above. But the same MHA requirements apply to smaller buildings, too, and the 9 percent inclusion rate would knock down the return on investment by about 30 percent—enough to kill many projects that would otherwise be feasible today (see pro forma tables in the appendix for results on NC65 under the high-rise MHA requirements).

Adding to the downside, any new housing development so much smaller than what zoning would allow is a 100-year lost opportunity twice over. It’s a loss for affordability simply in terms of fewer new homes to ameliorate Seattle’s housing shortage. And it simultaneously compromises the city’s planning goals to concentrate new high-density housing near the U District’s future high-capacity transit station, the primary reason for pursuing high-rise upzones in the first place. Using the two prototypes analyzed here as examples, every time a new apartment is underbuilt to 65 feet instead of 240 feet, the city loses the potential to gain another 166 homes without consuming any extra land.

Eventually, rents in the U District will increase enough such that high-rise housing development will start to reliably pencil. Will that take five years? Ten years? More? It’s difficult to predict, and land values and construction costs will rise over time as well. The 2021 opening of the Link light rail station will make the neighborhood more desirable and accelerate upward pressure on rents. Also, as rents escalate, the absolute return that a large high-rise project can yield will start to eclipse smaller mid-rise projects, boosting relative feasibility. In absolute terms, a 15 percent return on a $200 million dollar project is three times bigger than a 20 percent return on a $50 million dollar project.

Without MHA, many high-rise projects would likely pencil once U District rents have risen to the city’s high market-strength benchmark. But if subjected to the exaction imposed by MHA as it is currently proposed, that higher rent benchmark is still likely to be a mixed bag for high-rise development: a significant share of projects won’t justify investment, impeding homebuilding and thwarting the city’s affordability and transit-oriented development goals. All told, stalling high-rise homebuilding until rents “get there” is a backslide that will permanently widen the gap between homes available and people who want to live in Seattle, a gap that will hit hardest those residents with the least.

How to fix it: Less is more

Like the NC65-to-NC75 MHA upzone I analyzed previously, the MHA mandates on high-rise in the U District are simply too high. And they are too high for the same reasons. City planners are using more guesswork than analysis.

MHA has a sweet spot. If the mandates are pushed beyond it, the resultant loss of homebuilding feasibility means the policy will be worse for affordability than doing nothing.

MHA has a sweet spot. If the mandates are pushed beyond it, the resultant loss of homebuilding feasibility means the policy will be worse for affordability than doing nothing. Under these circumstances, dialing back the mandate to the sweet spot will deliver more subsidized homes and more market-rate homes. Counterintuitively, less yields more. The present analysis indicates that the proposed MHA rezone for SM-UD240 needs exactly that sort of correction.

How much of a mandate reduction is warranted? For a precedent, we need look no further than the city’s MHA proposal for high-rise zones in downtown and South Lake Union (SLU). The MHA requirements for downtown and SLU were negotiated as part the “Grand Bargain” compromise hammered out between private developer interests, nonprofit affordable housing providers, and city officials. Achieving this compromise necessarily hinged on MHA requirements that all parties could recognize as generally well balanced.

The proposed MHA inclusion rates for high-rise upzones in downtown and SLU range from 2 to 5 percent. While many of the downtown/SLU upzones are relatively small, certain zones in SLU would allow net capacity increases under MHA that are comparable in scale to the SM-UD240 upzone (see appendix for details). These particular SLU upzones require 4 percent inclusion or an in-lieu fee of $10 per square foot. At the same time, rents in downtown and SLU are the highest in the city, so certainly the U District deserves an MHA requirement no higher than 4 percent or $10.

For the SM-UD240 high-rise apartment example I discussed above, 4 percent inclusion in a high market-strength area yields a return of 12 percent. That’s down a bit from the 15 percent baseline, but on the plus side, the absolute return is $15.6 million compared to $9.1 million for the NC65 project. For the highrise example, dropping the inclusion rate from 9 to 4 percent would yield 15 affordable homes instead of 34. But 15 is better than zero, which is what Seattle would most likely get under the current MHA proposal.

To assuage concerns that the requirements would become too lenient as rents climbed over time, the city could consider a provision tying the metrics to rent inflation or for a performance review at given intervals. In Seattle’s political climate, once the MHA mandates are established, raising them will always be easier than lowering them.

Getting to the MHA sweet spot—now

High-rise construction is a paradox. It enables efficient use of urban land but is also inherently expensive. If Seattle hopes to reap the benefits of high-rise housing in neighborhoods such as the U District where the economics are challenging, policymakers must avoid trying to squeeze too much out of MHA. Unfortunately the feasibility analysis presented here indicates that MHA as proposed will inhibit high-rise homebuilding in a Seattle neighborhood where there is great transit access lots of jobs but where there aren’t currently enough places to live.

The solution? Lower the mandates to the level the math tells us is an MHA sweet spot, where we maximize production of both market-rate and subsidized homes so that a neighborhood like the U District can be a place for those who work and go to school nearby can actually live. Based on my feasibility analysis and the proposed mandates for high-rise in downtown and SLU, cutting the current U District high-rise requirements from 9 percent (or even 10 percent) to 4 percent or less is a prudent place to start.

Dialing MHA down to the sweet spot that produces more homes of all kinds may be counterintuitive but it makes all the difference between more inclusive or more exclusive neighborhoods. And the time to fix MHA is now, while it’s still a draft proposal and before it’s baked into the U District upzone. The alternative is an MHA mandate that will fail to deliver on its promise to leverage the city’s growth for affordability—that will, in fact, produce less housing than would doing nothing—and that will be vulnerable to legal challenge.

Next time: How does the draft MHA proposal measure up for the city’s low-rise multi-family zones?

Appendix

(Correction: This article originally included a statement about underbuilding at Yesler Terrace that was inaccurate.)

Pro forma input assumptions were taken from the city’s MHA feasibility study and are summarized in the two tables below. Based on feedback on my previous MHA feasibility article that the construction costs were too low compared to current norms, I raised concrete and wood frame construction costs by 10 percent, corresponding to the upper limit the city’s study applies in its sensitivity testing. I also increased the per-stall cost of underground parking from $35,000 to $40,000.

The city has not documented the estimated costs of the meeting the VIZ requirements under the proposed rezones, and the city’s feasibility analysis on the U District upzones apparently did not include the costs of VIZ. For this analysis, I assumed $5 per square foot payment on capacity above the FAR 4.75 baseline, based on the following examples. The proposed land use code (SMC 23.48.622) specifies that VIZ must compensate for 35 percent of the building capacity above the base. If the developer chose to meet the VIZ requirement through purchasing historic TDRs for $15 per square foot, that would translate to about a $5-per-square-foot payment on the capacity above base. If the developer chose to meet the VIZ requirement by building a public plaza at a cost of $105 per square foot, that would also translate to about a $5-per-square-foot payment on the capacity above base.

Pro forma data are given in the two tables below, one showing results for medium market-strength rents, and the other showing results for strong market-strength rents. Parameters defining the high-rise building prototype were taken from the city’s MHA feasibility study. The NC65 building was scaled to fit on the same size lot as the high-rise. To maintain consistency between the before-and-after MHA prototypes, the present analysis assumes a consistent parking ratio, as opposed to the single full floor of underground parking assumed in the city’s analysis.

Pro forma data are given in the two tables below, one showing results for medium market-strength rents, and the other showing results for strong market-strength rents. Parameters defining the high-rise building prototype were taken from the city’s MHA feasibility study. The NC65 building was scaled to fit on the same size lot as the high-rise. To maintain consistency between the before-and-after MHA prototypes, the present analysis assumes a consistent parking ratio, as opposed to the single full floor of underground parking assumed in the city’s analysis.

The number of required affordable units was based on an assumption that all of the increased development capacity granted by the upzone would go to residential use (the retail floor space remains constant on both buildings). Because the math never yields an exact integer number of required affordable units, the leftover fractional part of a unit was converted to an in-lieu fee, according the city’s method, documented here.

The pro forma results reveal that the in-lieu fee option becomes more attractive as rents and construction costs rise. This relationship is inherent to the math the city uses to convert between the inclusion percent and the in-lieu fee, and it is reflected in the city’s assumption that 90 percent of projects in downtown and South Lake Union will opt to pay the in-lieu fee.

In addition to return on investment, the pro forma tables below also show yield, which is the building’s net operating income (NOI) divided by the total cost of developing it. A rule-of-thumb target for yield is 6 percent. A drop in yield of just one- or two-tenths of a percentage point can flip a project from “go” to “no-go.” The yield results are qualitatively similar to the return results.

Regarding the comparison to MHA upzones in downtown and South Lake Union, for zones that currently have VIZ, meeting the MHA requirements grants the developer 60 percent of VIZ capacity above the base. Developers earn the remaining 40 percent by providing other amenities or by paying the in-lieu fee. While the MHA upzones tend to be relatively small, the VIZ capacity is often quite large. After this 60/40 split, in the case of three upzones, MHA requirements—4 percent inclusion or $10 per square foot—are “paying” for capacity boosts of around 100 percent, roughly similar in scale to the 72 percent boost (111 percent times 0.65) of the SM-UD240 upzone.

Jim

Why is land cost a constant in this analysis? Wouldn’t costs like MHA put negative pressure on the land price? Putting it another way, what happens to the price of land if you consider an output, rather than an input to this equation — whatever is left over after ALL costs (including MHA) + reasonable profit.

Phil BD

Great question that if unaddressed undermines this whole argument. Land is I think 10 or 15 percent of the cost of a typical high rise, so at some point lower land prices can’t compensate for all regulatory costs, but the effect needs to be considered.

Dan Bertolet

Thanks for your comments, Jim and Phil. It’s a question that comes up a lot. Here’s the reply I posted on my previous MHA article:

We discussed the land value adjustment question at length here:

http://www.sightline.org/2016/11/29/inclusionary-zoning-the-most-promising-or-counter-productive-of-all-housing-policies/

Added costs on development will no doubt result in developers bidding less for land, but when people get offered less for their property they will be less likely to sell, and if they don’t sell, then no new housing gets built.

Or another way to think about it: For someone who already purchased a property, if the added MHA costs make leaving the property in its current use more valuable than redeveloping it into housing, then that same math will make it more valuable to keep the property than sell it to someone who can only offer a land price that’s low enough to make housing development pencil.