")

")

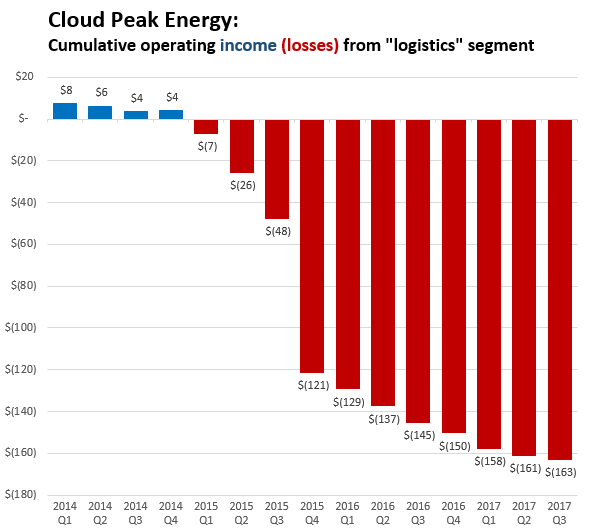

Cloud Peak Energy—a company that once put Asian coal exports at the center of its corporate growth plans—released its quarterly earnings last Thursday. And yet again the company reported some rather gloomy news about its coal export business: for the eleventh consecutive quarter, Cloud Peak’s export arm lost money. The loss was small: just under $2 million. Still, it added to the tide of red ink that has all but scuttled the company’s ambitions to refashion itself as a major player in the Pacific Rim thermal coal market.

All told, Cloud Peak’s “logistics” business—which is dominated by exports—has racked up more than $160 million in operating losses since the beginning of 2014:

Why all the red ink? In a nutshell, Cloud Peak made a series of huge and disastrous bets on Asian coal exports, just as Asian coal markets were tanking. The company paid tens of millions of dollars to secure port space and rail access at the Westshore coal terminal in southwest British Columbia, locking in so-called “take-or-pay” contracts that obligated the company to ship coal even if it cost money. And the company’s top brass spent millions more to support new export terminals in the Pacific Northwest. On its balance sheets, the company treated these payments as long-term “assets” that would eventually prove profitable. But as Pacific Rim coal prices collapsed and export profits evaporated, Cloud Peak’s accountants had no choice but to admit that the company’s export “assets” were actually worthless. To add insult to injury, the company ultimately paid rail and port companies hefty fees to extract itself from its long-term shipping contracts—fees that continue to weigh down the company’s export results.

To make matters even stranger, one piece of Cloud Peak’s export strategy actually yielded a hefty profit over this period. Earlier this decade—before the Asian coal bubble fully deflated—the company cleverly adopted a “hedging” strategy, buying futures contracts that would gain value if coal prices fell. Between 2014 and 2016 the company realized a gain of nearly $50 million on those contracts. Unfortunately for Cloud Peak, there’s only so much money that a coal company can make by betting that coal prices will collapse.

In their quarterly call with investors, Cloud Peak executives tried to put a rosy face on the company’s export losses. First, they emphasized an “adjusted” measure of earnings—one that ignores the money the company has spent to restructure its export contracts. Second, they suggested that the recent uptick in Asian coal prices could lead to better financial results over the next few quarters. They could be right about that…but a quarter or two of export profits won’t compensate for the brutal losses the company’s export division has racked up over the last few years.

And if you listen closely, you can hear that Cloud Peak’s top brass now views their big bet on exports as a costly albatross. When asked whether the company would extend its export commitments for an additional year, Cloud Peak’s CEO said:

[W]e will be very cautious about not taking on too much take or pay risk. We’ve sort of learnt our lesson on that.

And what an expensive lesson it was.

Comments