Sightline is releasing a new report today—Unfair Market Value II: Coal Exports and the Value of Federal Coal—documenting massive exports of federally owned coal over the last decade. The US Bureau of Land Management (BLM) sold private companies the right to mine this coal for a pittance—in some cases, for less than 20 cents per ton. And when Asian demand was red-hot, these companies made massive profits selling millions of tons of federal coal overseas. Nonetheless, BLM has essentially ignored export economics when setting the “fair market value” that it will accept for federal coal leases. Now that the Department of Interior has placed a three-year moratorium on new coal leases pending a thorough review of federal coal policies, BLM has an ideal opportunity for a thorough review of the economics of exports. And our report points to evidence that by ignoring exports, the BLM has been selling many federal coal leases at just a fraction of their true economic value.

Below is a brief synopsis of our findings.

If you’ve been following the news, you probably know that coal is down in the dumps. Three of the top five US coal companies have declared bankruptcy in the past year, part of a massive trend of insolvency sweeping the industry as solar, wind, and natural gas steadily eat into coal’s market share.

But it wasn’t that long ago that King Coal was riding high. From 2010 through 2013 international coal markets glowed red hot as soaring Chinese demand pushed prices into the stratosphere. That’s when the promise of massive export profits spurred US coal companies to take on massive debts to buy export-oriented coal businesses. And it’s also when those companies began their quest to build coal terminals in the Pacific Northwest, which offered the cheapest and most direct route from the massive coalfields in the US West to the energy-hungry economies of the Pacific Rim.

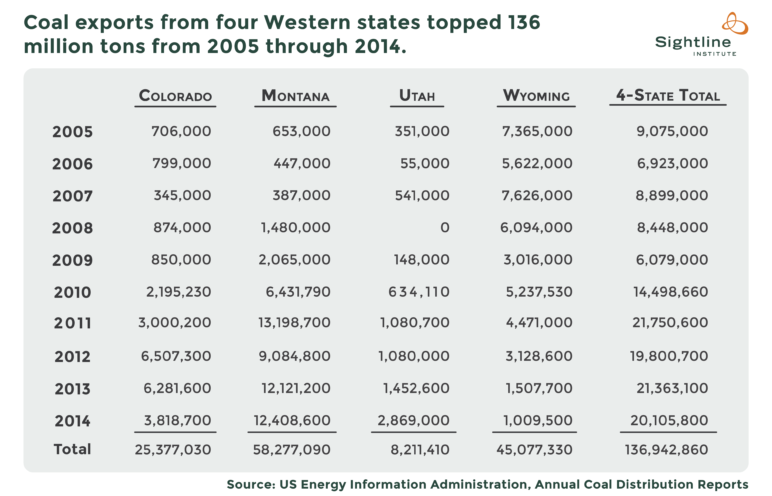

During the height of the Asian coal bubble US coal companies took full advantage of high international prices by shipping tens of millions of tons of coal overseas—often earning phenomenal profits in the process. Many of those exports originated in mines in the western US; from 2005 through 2014, the states of Colorado, Montana, Utah, and Wyoming shipped a combined 136.9 million tons of coal to overseas customers, with a huge spike beginning in 2010, just after China’s demand for imported coal started to skyrocket.

As our new report shows, much of the coal that US coal companies shipped overseas was originally owned by the American public. Acting on behalf of We the People, BLM sold the right to mine that coal for almost inconceivably low prices, sometimes as low as 18 cents per ton. And at the height of the Pacific Rim coal bubble, those companies could turn around and sell the coal at lofty prices, earning up to 80 times as much in profit as they paid for the coal in the first place.

For a while, exports offered profits that coal executives could only dream of in domestic markets. Yet despite ample evidence that the coal industry has used federal coal leases to develop export-oriented coal mines in the western United States—mines that are well-suited for exports but have far more modest domestic prospects—BLM has largely ignored the economics of coal exports when deciding the “fair market value” at which it will sell federal coal leases. But as the Asian export boom showed, they should have been paying closer attention: BLM’s coal leasing practices led to substantial windfall profits for coal exporters at the expense of the American public.

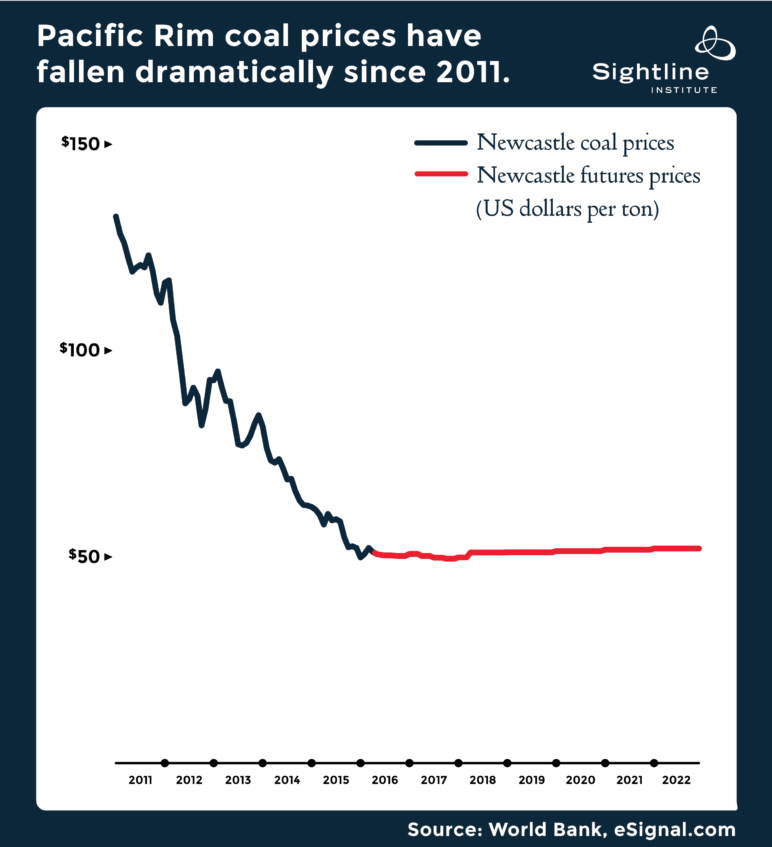

Of course, the good times for coal exports didn’t last. Sky-high prices pulled all sorts of new coal projects into the pipeline, even as China’s coal consumption slowed. Starting in early 2011 seaborne coal prices started to fall…and kept falling for 5 straight years.

As prices fell, export profits shrank, then turned into a trickle of red ink, and finally a torrent…leading many coal companies to curtail their export activities. And the futures market doesn’t hold out much hope for a rebound.

But the fact that export markets are in the dumps right now doesn’t mean that BLM should ignore exports when setting coal leasing policies. Coal leases are good for at least a decade, and usually more—which, in theory, is plenty of time for another coal bubble to re-inflate, once again yielding massive windfall profits for the coal industry.

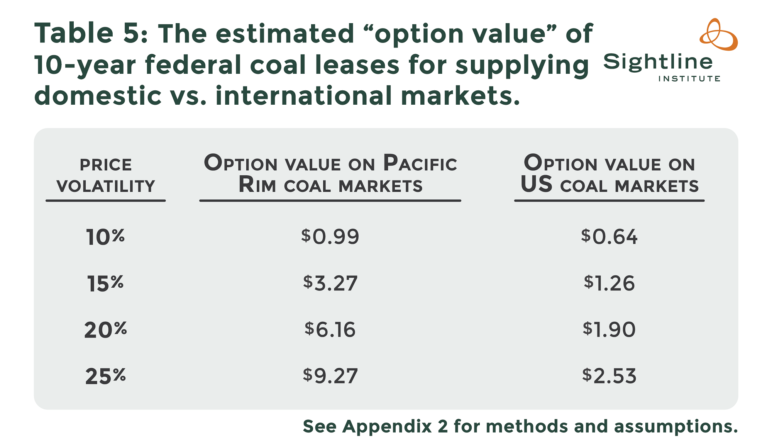

And as a growing body of academic research and real-world practice shows, owning the rights to coal reserves can give coal companies the ability to profit from price increases, without obligating them to incur losses if mine development looks unprofitable. As it turns out, the right to earn a profit without risking a loss can be worth quite a bit. There’s an entire field of financial economics known as “real options theory,” devoted to estimating the value of speculative projects such as coal mines. We’ve run the numbers, and estimate that even in today’s dismal export market, owning the right to profit from future price increases in export markets could be worth more than $9 per ton.

As the chart above shows, even in today’s down market coal leases are worth much more than the federal government has sold them for. Just as importantly, the high prices and wild price swings in export markets can make exports more valuable than domestic sales.

Which is all the more reason for BLM to look at the economics of coal exports when deciding the price it will accept for federal coal.

Read Sightline’s full report, Unfair Market Value II.

Why sell coal to burn to cause climate change when the best case is about $200 million in payments to the US Treasury?

And shipping coal to Pacific ports is disruptive to the communities along the rail lines that would need to carry far more coal trains if this were to take place, yet the coal industry claims that mitigating that harm is too expensive because of all the workers who would need to be paid to prevent the disruption.

So, creating jobs is counter to the interests of the coal industry who demand everyone affected just suffer the costs of coal in their lives.

So, Western government coal won’t solve any government revenue problem nor create that many jobs because paying workers costs too much.

Leave it in the ground and put people to work building wind and solar farms and batteries and power lines. Which unlike coal, will last for decades and generate revenue bit by bit for decades to pay the workers steadily over decades as they build out and then maintain and replace them over the centuries.

Ok, here’s the deal. China is going to do whatever it wants. They dont care about your envirowacko agenda. Now, if we were to ship coal that has lower sulphur and higher BTUs, China’s pollution and CO2 emissions WILL go down. Isnt that a good thing? Right now they are burning synthetic natural gas. Great for the smog, REALLY high CO2 emissions. So shipping coal overseas is a win/win for now.

The Federal gov’t doesn’t charge “market value” for key natural resources. Coal, oil & gas, grazing rights, and timber are all resources extracted from Federal lands at a fraction of what they cost to extract from private land. Taxpayers subsidize the entities using these resources. To whom is that fair?