Today, Sightline is releasing a new report: Peabody Energy, Gateway Pacific, and the Asian Coal Bubble. The report shows that at today’s prices, there’s no way for Peabody to make money shipping coal to Asia. Peabody’s strategy is now to hope that the Asian coal bubble re-inflates—which is an increasingly risky bet, given the collapse of Asian coal prices, recent steps by China to curb coal demand, and the oversupply of coal from other Pacific Rim exporters.

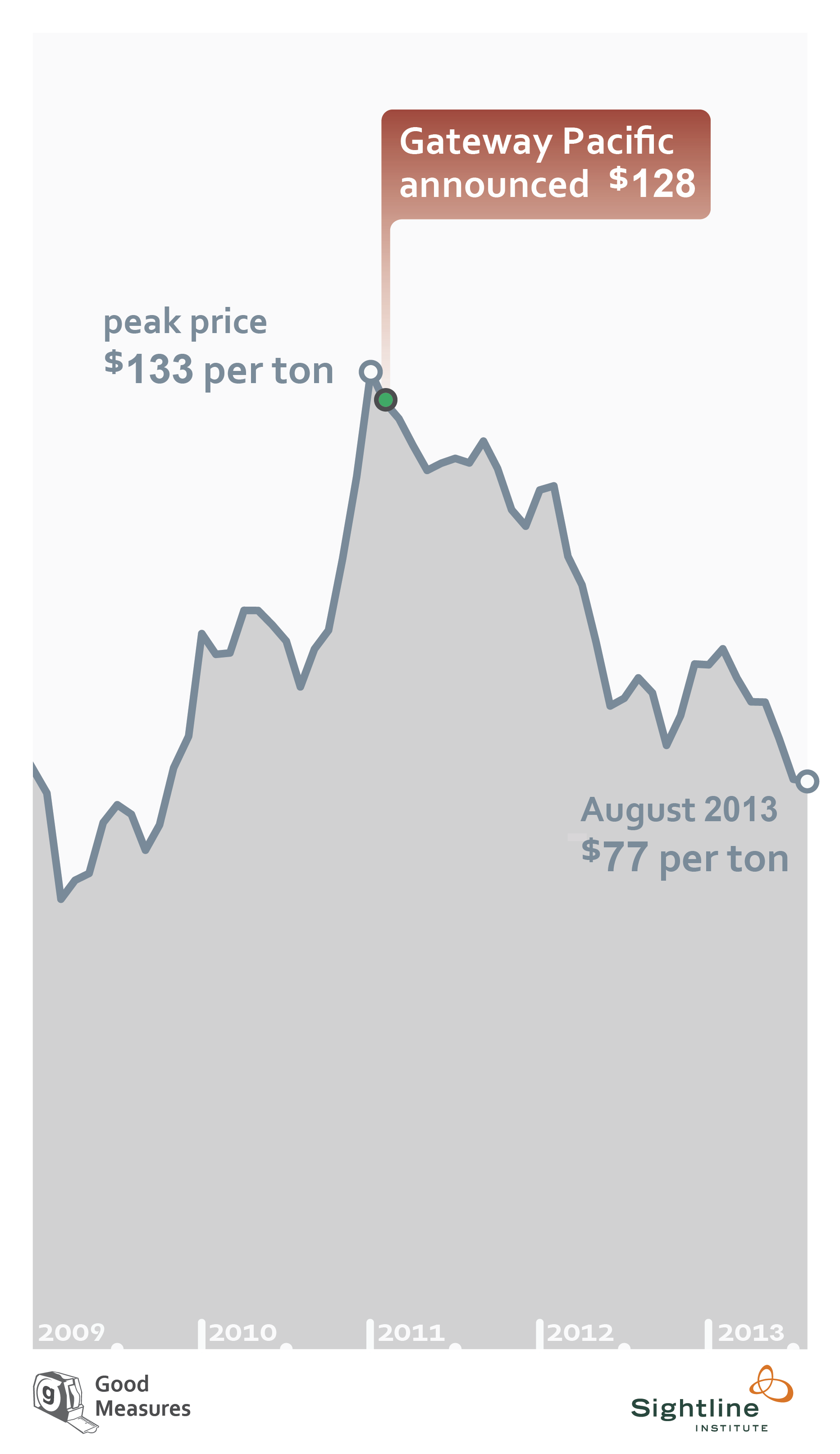

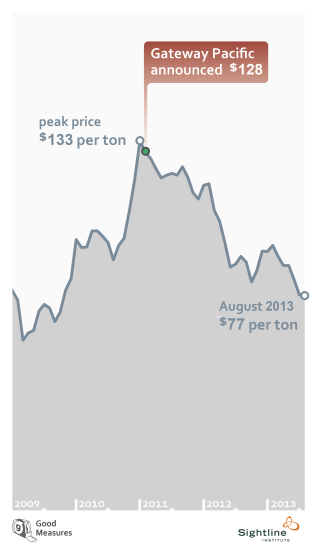

In case you don’t happen to check the price of Australian coal every day, you might not have noticed that the price of coal in the Pacific Rim export markets has collapsed over the past year or so. In fact, it’s looking very much as if the meteoric rise in coal prices that enticed so many companies to enter the Northwest coal export game was simply a bubble.

And perhaps no Powder River Basin coal company has more at risk from this collapse than Peabody Energy.

Peabody has plans to export up to 24 million metric tons of coal each year through the proposed Gateway Pacific terminal in northwest Washington. It announced those plans in February 2011—about two years after Pacific Rim coal prices started to spike but a month after they peaked.

Since Gateway Pacific was launched, Pacific Rim coal markets have fallen almost as quickly as they rose. At today’s prices, Peabody Energy would lose roughly $10 per ton selling coal through the Gateway Pacific terminal.

Sightline’s new report, Peabody Energy, Gateway Pacific, and the Asian Coal Bubble, tallies the costs for Peabody to ship its coal from the Powder River Basin to Asia—including the cash costs of mining coal, rail shipping fees, handling fees at coal terminals, shipping costs on ocean-going vessels, and adjustments for the low energy content of Peabody’s Powder River Basin coal.

The conclusion is clear: in today’s market, there is literally no chance for Peabody to make a profit on coal exports.

Read more