Oil train derailments—and the catastrophic fires that often result—are distressingly common features of contemporary North American life. No fewer than 10 crude oil-bearing trains have derailed and exploded since the summer of 2013. The risks to life and limb are plain enough. Less understood is the risk that these oil trains pose to taxpayers, governments, and public budgets.

No railroad in North America carries anywhere close to a level of insurance proportional to the financial risks of hauling oil. It’s a problem that is most pronounced with the small and regional railroads that often transport oil on the last leg of its journey from well to terminal. And it’s a problem that is acute in the Pacific Northwest, where a radically under-insured company called Genesee & Wyoming (G&W) aspires to enlarge its already significant role in crude oil movements.

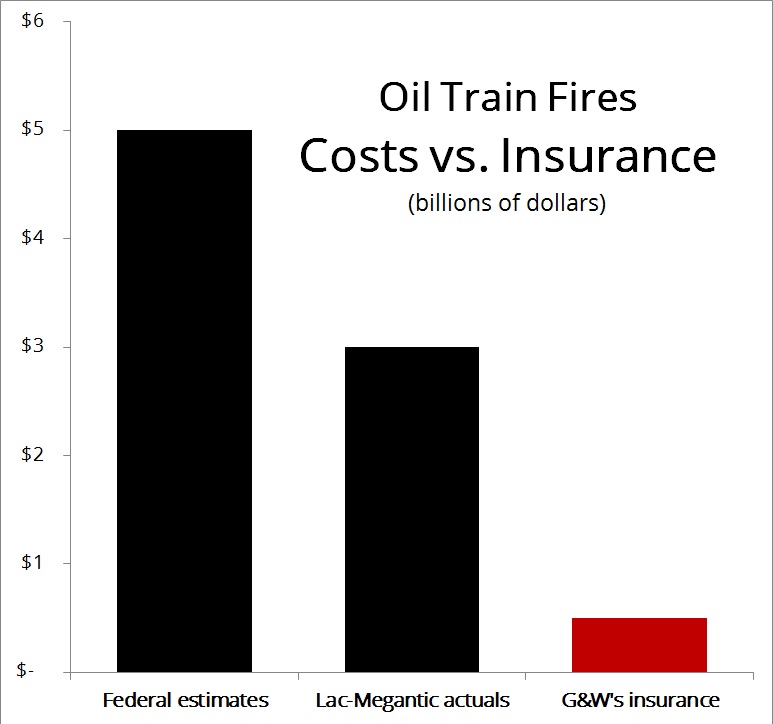

G&W’s huge insurance gap poses a direct financial risk to taxpayers.

G&W’s Portland & Western line is permitted to haul 12 trains worth of oil per week through Columbia County, Oregon, to a terminal on the Columbia River near Clatskanie. Plus, if Washington regulators approve three proposed oil terminals in Hoquiam, Washington, the firm’s Puget Sound & Pacific line could haul roughly 17 trains weekly through Grays Harbor County to the port.

Yet G&W is severely under-insured against the threat of oil train derailments and fires. Officials estimate that the total cost for rebuilding and cleaning up Lac-Mégantic, Quebec—a small town of only about 6,000 residents that was hit by a major oil train fire in 2013—is a staggering $3 billion over the next decade.

But the costs of an oil train derailment could be even greater than that. Sightline’s review of regulatory proceedings, actuarial findings, and legal settlements finds that a reasonable worst-case scenario oil train derailment in a Northwest city could cost $5 billion or more.1

G&W carries at most $500 million in liability insurance to cover its entire suite of railroad holdings—of which the two Northwest lines comprise only a small fraction. In fact, even liquidating the firm’s total net worth of $2.1 billion in bankruptcy to pay for damages might not be sufficient to cover the cost of a mishap.

G&W’s huge insurance gap therefore poses a direct financial risk to taxpayers—especially those in Northwest communities such as Grays Harbor County, Washington, and Columbia County, Oregon.

And G&W is no stranger to oil train explosions. In fact, the company’s tracks hosted the second-ever catastrophic oil train derailment and explosion in November 2013 when a 90-car crude oil train derailed on a trestle near Aliceville, Alabama. The damaged rail cars erupted into fireballs and spilled substantial quantities of oil into a wetland.

Adding insult to injury, G&W refuses to disclose its insurance coverage levels to the public or government regulators. Decision-makers therefore have no way to evaluate the financial risks posed by the construction and operation of oil train facilities, such as the three proposed for the Port of Grays Harbor.

Not only are insurance levels wildly inadequate to the risks, but the industry obstructs public understanding of even basic information about railway liability exposure.

In the course of studying railroad insurance shortfalls, Sightline Institute contacted G&W’s corporate offices directly. A representative of the firm told us that they would not disclose information about their insurance coverage for major catastrophes. Sightline also attempted to contact the Environmental Manager of the Columbia Pacific Bio-Refinery in Columbia County, Oregon, a facility that currently receives crude-by-rail from G&W, but we received no response to multiple emails and phone calls.

We examined published documents about the railroad. As a publicly traded company, G&W must disclose certain kinds of financial information to the US Securities and Exchange Commission (SEC). Sightline reviewed G&W’s SEC filings and other legally required disclosures, but we were unable to identify to identify any relevant disclosures that would shed light on railroad liability insurance levels.2

Sightline reviewed dozens of publicly-available materials, including regulatory proceedings, testimony to Congress and federal agencies, government research reports, legal briefs, media accounts, and more. We conclude that large “class 1” railroads like BNSF—North America’s dominant rail hauler of crude oil—may have somewhere in the range of $1 to $1.5 billion in insurance coverage while smaller railroads like G&W almost certainly have much less. For example, a 2009 report from the US Department of Transportation that examines insurance, security, and safety costs for railroads quotes representatives of the American Short Line and Regional Railroad Association saying, “Class II and III railroads… only maintain $10 to $100 million in coverage.”3

G&W may have more coverage than most small railroads: as much as $500 million worth, according to one industry media account in 2013. Yet Sightline was unable to corroborate this figure, and based on our research, we believe it likely represents an upper-end estimate of the firm’s coverage.

Sightline is hardly alone in failing to uncover hard numbers on railroad insurance levels. Even the US Transportation Department acknowledges that the federal government is unable to confirm insurance data with the railroad companies or their insurers.

The acute lack of information is a serious problem for an industry hauling explosive crude oil through cities and towns. It means that communities are blind to financial risks that could bankrupt them, risks that are foisted upon them by railroads.

In its 2014 Draft Regulatory Impact Assessment, a study prompted by the spate of alarming oil train explosions, federal regulators characterized insurance limitations as a “market failure.” Yet more than a year later, there are still no plans to correct it.

Railroad expert Fred Millar contributed research and analysis to this article.

1 Sightline’s estimates of railroad accident costs may be far too low. In 2013, Union Pacific petitioned the Surface Transportation Board for a declaratory order requiring shippers of Toxic-by-Inhalation-Hazardous material to indemnify UP against all liabilities, other than those resulting from UP’s negligence or fault. The petition was eventually rejected, but Assistant Vice President for Finance and Insurance Warren B. Beach gave testimony regarding the difficulty railroads face in insuring hazardous cargo: “UP had commercial liability insurance totaling $1 billion as of 2008,” and that although typical maximums are around $1 billion, “in 2012 UP was able to purchase $1.2 billion of commercial liability insurance… the potential loss from a single terrorist attack involving release of hazardous materials in a heavily populated area can reach hundreds of billions of dollars. Thus, even if UP could double or triple its coverage, it would not come close to covering the potential loss for a truly catastrophic event.”

2 The nearest information pertains to self-insured retentions and casualties and insurance coverage, an unrelated (and much smaller) type of policy that railway companies carry. According to G&W’s SEC filings in 2014, the firm’s liability policies had self-insured retentions of up to $2.5 million per occurrence. (A self-insured retention is an amount that must be paid by the insured party to the claimant before the insurance coverage begins. Since it is paid to the claimant, it differs slightly from a deductible.) We also know that G&W paid $41.5 million in 2013 and $38.5 million in 2013 for Casualties and Insurance coverage. Unfortunately, insurance experts like Daniel Roddy at HMBD Insurance Services assured us that there is no way of estimating total insurance coverage based on monthly payments or self-insured retentions without much more information and the help of underwriters.

3 The report states that “while $1 billion is more than sufficient to cover losses from ‘routine’ [Toxic Inhalation Related]-related incidents, it is well short of the $5 to $6 billion that Class I railroads estimate would be necessary in a ‘nightmare scenario.” Estimated costs from a catastrophic crude oil train derailment in an urban area are similar. Representatives from ASLRRA also explained that “small railroads cannot afford premiums for ‘meaningful’ amounts of insurance coverage… Class II railroads would likely be content with $200 million in coverage and Class III carriers would likely be satisfied with $100 million in coverage…While there is sufficient capacity within the rail insurance market to satisfy this demand, many short line haulers simply do not have the cash-flow to pay for such insurance coverage.”

Under public questioning Mr. Haka, G&W Vice President, told a meeting of the Port of St. Helens Commissioners that his company’s coverage is $400 million.

Does the insurance coverage include damage to humans as well as environment? Or is the insurance coverage discussed used to cover something else?

Yes, the insurance coverage I’m referring to would be for basically everything—people, property, and the environment.