")

")

The centerpiece of Seattle’s Housing Affordability and Livability Agenda (HALA) is an innovative policy called Mandatory Housing Affordability (MHA). Exemplifying HALA’s core principle of leveraging growth for affordability, MHA promises to fulfill almost a third of the city’s ten-year goal to produce 20,000 affordable homes.

To get there, though, MHA must play nice with the unpredictable and dynamic world of private real-estate development, and that calls for a cautious approach to setting the program’s parameters. Getting it right will be like shooting an apple off someone’s head with a shotgun: you’d better aim high. Oh, and the person with the apple is also dancing.

At the same time, the populist impulse to demand more affordable units, combined with the anti-growth impulse to oppose larger buildings, will create political pressure for more stringent MHA requirements—as if someone’s pulling down on the barrel of that shotgun as you’re trying to aim. Hyperbole? Read on.

What is MHA?

Seattle’s MHA approach can become a model for growing cities in Cascadia and beyond.

MHA couples affordability mandates on private development with zoning changes that allow the construction of taller buildings. If it works, the city scores a win-win of more market-rate housing and more subsidized affordable housing. But if policymakers push the requirements beyond what homebuiding economics can support, they risk the lose-lose outcome of no new housing at all.

Seattle Mayor Ed Murray recently unveiled the MHA framework, which lays out preliminary targets for the number of apartments affordable to low-income households that developers must include in new housing projects. It also proposes fees that developers can pay in lieu of providing those units that Seattle’s Office of Housing would then use to fund affordable housing built elsewhere. Over the next six months, planners will engage real-estate economists to refine those parameters. In parallel, the city has launched a public process to define the appropriate changes to zoning.

Beyond the metrics, the MHA dialogue has already begun to catalyze an unprecedented political alliance between the social justice community and urbanists, along with a corresponding marginalization of those advocating for tighter limits on new housing. Over the long run, this cultural shift may prove more important than the policy itself. But the success of both will hinge on implementation driven by data, not politics. If policymakers can pull that off, Seattle’s MHA approach can become a model for growing cities in Cascadia and beyond.

The balancing act, part 1: Feasibility vs. affordability

Creating new affordable housing through MHA completely depends on risk-taking private developers—no private development means no new subsidized homes. And the catch is, restricting rents to below the market rate reduces a building’s revenue-generating potential, undermining the feasibility of development. This isn’t about greedy developers getting mad, taking their ball, and going home. Banks won’t grant the large loans needed to fund apartment construction if the projected returns are too low.

Accordingly, city policymakers aim to set up a balanced system in which a zoning change that allows the construction of a larger building—an “upzone”—offsets the financial burden of fulfilling the affordability mandate. A larger building makes room for additional market-rate rentals that generate extra revenue to cover the losses on the below-market-rate units (or the cost of the in-lieu fee if the developer chooses that option).

If policymakers can strike this balance, MHA will have no impact on feasibility. Development projects will move ahead at the same pace as they would have without MHA, but they will yield subsidized housing as well as additional market-rate housing. Matching the cost of the mandate with the value of the upzones will also keep MHA on the right side of the law: by most interpretations, Washington prohibits such financial penalties on private property without compensation.

But the balance is extremely delicate. Development feasibility depends on numerous factors, including interest rates, real-estate cycles, neighborhood market strength, land values, building type, site-specific conditions, permitting uncertainties, and construction costs such as wages and materials. These factors shift over time, sometimes quickly.

Given this unpredictable morass of variables, Seattle would be prudent to err on the side of lower mandates. Because when feasibility is close to the brink, the financial hit caused by a requirement for too many below-market-rate units could tip the scales and kill a project altogether, which, it’s worth repeating, means no new market-rate or affordable homes for anyone. The city’s challenge will be to resist the inevitable political pressure to escalate the affordability mandates, so as to avoid killing the golden goose of private development.

The balancing act, part 2: Upzones vs. upset

On the opposite side of the MHA equation are the upzones that allow taller or bulkier buildings. And therein lies the second layer of challenge: political pushback against larger buildings. Just as hiking the affordability mandates could kill development, so could shrinking the upzones. Likewise, given all the uncertainties involved in real estate development, the city would be smart to err on the side of generous upzones. As a starting point, the 2015 HALA report included recommendations for upzones, most of which raise allowed building heights by one story.

Untangling the complexities of MHA and establishing a system that keeps the golden goose alive will not be easy. Most critically, policymakers must not overlook the basic fact that private development is a game of risk and probability, and any financial penalty that reduces the potential return on investment will reduce the likelihood of new housing getting built—market-rate or affordable. In a city with an affordability crisis caused by a housing shortage, imposing new regulations that impede the construction of housing is like cutting off a farmer’s water supply during a famine.

On the other hand, if Seattle can strike the right balance and enact upzones that otherwise would never have passed political muster, the payoff will be big: much more housing, and more of it affordable.

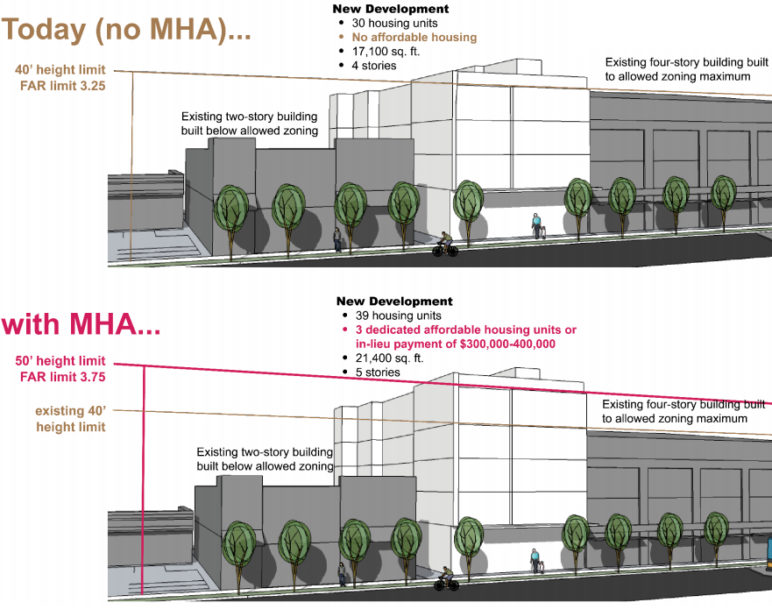

City of Seattle diagram illustrating how MHA would allow the addition of a fifth floor to a four-story building in exchange for the provision of three below-market-rate units or an in-lieu fee payment in the range of $300,000 to $400,000. A measure of development intensity, FAR (floor-area-ratio) is the ratio between the total floor area in the building and the area of the property it is built on. By City of Seattle, used with permission.

The MHA weeds

For those readers comfortable crawling deeper into the weeds of MHA, it’s safe to keep reading. Others, you have been warned.

What follows is one straightforward method for assessing the impact of MHA on development feasibility. We start with a base assumption that the developer has already secured a project that is feasible under current regulations and zoning. We then ask, if the city imposed a given requirement to provide below-market-rate units along with a corresponding upzone, would the rent income from all of the additional units cover the cost of building them, including a reasonable return on the investment?

If yes, then feasibility is not compromised and the enlarged project will yield below-market-rate apartments, as well as a greater number of market-rate units than the base building would have included. If no, then the policy is likely to do more harm than good by impeding the development of new housing.

Penciling out the on-site affordable units option

As a test case, let’s try the example project described on page 20 of the Director’s Report on the MHA framework. It’s a 255-unit apartment building for which an upzone granted an increase from five to six stories. The proposed mandate is that 6 percent of the building’s total units must be affordable to households earning up to 60 percent of area median income (AMI), for a period of 50 years. That translates to 15.3 below-market-rate units, leaving room for an additional 27.2 market-rate units in the remainder of the new space created by the upzone (for this estimate we can ignore that the unit counts are fractional).

The feasibility modeling requires the inputs given in the table below (see the notes at the end of the article for definitions and sources). Applying these assumptions, rent revenue from the added units minus the cost of operating them—the “net operating income” (NOI)—is $557,000 per year. The annual cash flow to both cover the expense of building the additional floor’s worth of units and also achieve a 6 percent return on investment is $554,000, or just 0.6 percent less than the NOI. In other words, under this scenario the MHA parameters are almost perfectly balanced. The project remains feasible—it’s in the policy’s sweet spot.

MHA Feasibility Modeling Assumptions

| Market Rent | $2.80/sf |

| Rent for 60% AMI | $1.60/sf |

| Operating Expense | $0.92/sf |

| Turn-key Development Cost of Added Floor | $236/gsf |

| Rentable Floor Area Efficiency | 0.82 |

| Required Project Yield | 6.0% |

| Inclusionary Unit Requirement | 6.0% |

| In-lieu Fee | $12/gsf |

However, modest changes can push the project out of that sweet spot. For example, if construction costs rose by 20 percent—common during boom times—the annual cash flow needed to cover construction of the extra units is $107,000 more than the NOI from those units. If instead, the below-market-rate requirement was doubled from 6 to 12 percent, the cash flow to cover construction would remain the same, but the NOI would drop by $166,000 per year.

If on top of that, the rent restriction was deepened to provide affordability for 30% AMI households ($0.80/sf rent), the NOI would take a total hit of $385,000, equivalent to a 9 percent reduction of NOI for the whole building. For any such scenario in which the MHA requirements cause the dollar signs to go substantially negative, developers will be less likely to pursue the project, jeopardizing the production of any housing at all.

Penciling out the in-lieu fee option

If the developer of our example project opted to pay the in-lieu fee instead of building the below-market-rate units, the proposed fee of $12 per square foot translates to a total fee of $2.8 million. In this scenario, the NOI and the annual cash flow necessary cover the cost for construction—which now includes the $2.8 million fee—remain very closely matched. That is, the choice between building the below-market-rate units and paying the in-lieu fee is a financial wash.

The merits of including subsidized units in a market-rate building versus collecting in-lieu fees that fund subsidized units built elsewhere is the subject of ongoing debate. But either way, their relative cost to a project under MHA depends on a sensitive equation. In our example, with an increase in market rent to $3.25 per square foot, the bottom line for the in-lieu fee scenario is about $60,000/year better than including below-market-rate units in the project.

Ready, aim…

Remember that apple target at the start of this article? The shotgun metaphor ought to make more sense now. Now to explain why I said the person is dancing: The example project analyzed above is complicated enough in itself, but it’s only one permutation among myriad building types and upzones for which the city must define MHA requirements. The task of setting these parameters in the stone of Seattle’s land use code is rife with the risk of oversimplification and loaded with potential for unintended consequences.

For example, small-scale projects are particularly problematic. How does a developer provide 6 percent affordable units in a project that only has eight apartments? And granting an additional floor on a townhouse isn’t likely to add much value because it won’t increase the number of homes that a builder can erect on a site. Small efficiency dwelling units, too, need their own set of unique requirements.

On top of the variability of the buildings themselves, to account for how market rents vary by location, planners have divided up the city geographically into three tiers. Based on the premise that higher market rents can support a bigger mandate, preliminary below-market-rate unit targets for the three tiers are five, six, or seven percent of total units. But this system introduces fairness issues at the boundaries between tiers and needs frequent updating to reflect evolving market conditions.

High-rise construction is another special case. To mesh with Seattle’s existing incentive zoning program, the MHA upzone cannot grant additional height. Instead it must allow buildings to have larger cross-sectional area—that is, to get bulkier. Furthermore, to make the math balance out with the higher construction costs of high-rises, planners are proposing below-market-rate unit percentages in the range of 2 to 5 percent, which is lower than the proposed range of 5 to 7 percent for buildings up to eight stories tall. An initial proposal showed that 35 different requirement sets were necessary to cover just the city’s high-rise zones.

The unruly complexity of MHA begs the question: is there a simpler solution? In an ideal world, a cleaner approach would be to adopt the same upzones recommended by HALA but replace the MHA affordability mandates with a citywide land-value tax. The land-value tax would capture the property value boost from the upzones, and its proceeds could pay for subsidized housing. Unfortunately, in our non-ideal world, land-value taxes face daunting legal barriers, while on the political side, few constituencies are likely to mobilize for such an approach.

…Fire!

An aim-high approach to setting the affordability mandates is the key to MHA’s success.

I’ve been harping on the risky shot before the architects of MHA not because I believe it’s hopeless. Rather, my intent is to emphasize that an aim-high approach to setting the affordability mandates is the key to MHA’s success.

Yes, if the mandates are too small—that is, if they are less demanding than they could have been without dampening development—the city will end up with somewhat fewer below-market-rate apartments. That outcome would be unfortunate though not disastrous, because the city would still get more market-rate apartments that absorb pent-up demand for housing and relieve upward pressure on prices. (HALA also has a ten-year goal of 30,000 market-rate units.)

But if the mandates are too large—if they are more onerous than the ever-shifting economics of housing construction will tolerate—the city stands to lose both new subsidized apartments and new market-rate apartments. And that outcome truly would be a disaster in a city where a shortage of housing is driving prices sky-high.

With MHA, Seattle has an unprecedented opportunity to create affordable housing while simultaneously building a new political bridge between two worlds: that of social justice advocates and non-profit housing developers and that of pro-density urbanists and private developers. If Seattle can successfully overcome both the technical and political challenges of implementation, MHA will not only put more housing on the ground but will also lay the cultural and political groundwork for ongoing progress towards growth with affordability.

Read: Eight ways exclusionary zoning makes our cities more expensive and less just.

Notes

The assumptions used in the feasibility model are based on input from local real estate development professionals.

- Market rent is for a typical, new, midrise apartment located in an area classified as “medium” market by the proposed MHA framework.

- Rent for 60% AMI is based on Seattle’s rent limit of $1,017 per month for a one-bedroom, assuming a unit with 650 square feet of rentable space.

- Rent for 30% AMI is based on Seattle’s rent limit of $504 per month for a one-bedroom.

- Operating expense is based on typical new Seattle apartments; subtracting operating expense from rent revenue yields the net operating income (NOI).

- The turn-key development cost of an added floor is the cost of building a sixth woodframe floor on a five-story project; the cost is lower than the typical development cost for an entire building mainly because it does not include the cost of land.

- Rentable floor area efficiency is the ratio of the building’s rentable square feet (doesn’t include floor area not used by specific tenants such as utility spaces) to gross square feet (the floor area of everything in the building).

- Required project yield is the return on investment lenders need to justify risking money on a project. For a project to “pencil,” the NOI must cover the yield. In Seattle’s current hot market, yields in the range of 5.5% are not uncommon, but we use 6% percent to represent more typical market conditions.

- sf = rentable square feet; gsf = gross square feet

Thank you to Kristin Ryan, Maria Barrientos, Ben Broesamle, Gabriel Grant, and Matt Hoffman for vetting the assumptions and results.

Erik

I’m no expert in these issues, but is it fair to say that if developers choose the in-lieu fee, this would basically lead to more socio-economic segregation within the city? I would think it would be nice if the deal was sweetened slightly for providing affordable housing in the same building, since that would help allow more choice in locations for people seeking those options. I’m assuming the funds from the in-lieu fees would be applied to other projects in other areas of the city instead of applied to a different project in the same neighborhood (perhaps a poor assumption?)

Tim Schriever

Mandatory affordability requirements will only create a plethora of regulations and more work for government staff. That great if you work for the government, but it will increase the cost of market rate housing and it will be unenforceable after the units are built. It may initially create a few more affordable units but will quickly digress to units being occupied by people who do not need affordability. Take the case of a young family with relatively low income that gains work experience and increases their income moving out of the low income category. The City should use incentives to create more affordability and change the existing zoning to allow an adequate number of housing units without trying to micro-manage the housing industry and occupants of the “affordable” units.

Sally

Copy what’s worked well elsewhere where high tech jobs pushed housing costs up. Trying to invent something new doesn’t work here. Look at the unique — and uniquely abusive — financing plan for Sound Transit. That’s the latest brainchild of government heads around here.

Bruce Meyers

Added height is not appropriate for all parcels. Neighborhoods with narrow streets, such as Ballard will h a very buildings and yards with shade most of the year. Taller buildings need to be stepped back from the street and from adjacent properties. Vancouver and Toronto has this type of design requirements, but Seattle planners continue to ignore how far north we are compared to almost any US city.

Bruce Meyers

Added height is not appropriate for all parcels. Neighborhoods with narrow streets, such as Ballard will have buildings and yards with shade most of the year. Taller buildings need to be stepped back from the street and from adjacent properties. Vancouver and Toronto has this type of design requirements, but Seattle planners continue to ignore how far north we are compared to almost any US city.