*** This is a preliminary summary of a huge bill, so it’s not Sightline’s final answer. Look for a more thorough and polished analysis next week. ***

Weighing in at 821 pages, the Kerry-Boxer climate bill introduced into the US Senate yesterday is officially a whopper, though it’s certainly more svelte than the companion House bill that it substantially mirrors. (Apparently, it’s Kerry-Boxer, not Boxer-Kerry, despite what you may have heard.)

Update, 1:20: quick aside on the price ceiling: Lots of folks asking what I think about the “price collar” approach in this bill, especially the price ceiling that appears to be a cap buster. In a nutshell: the price ceiling ends up being no worse than the quality of the program’s offsets. (By analogy, however, getting hit by a bus is no worse than getting hit by a truck!)

I’m officially not a fan of the price ceiling, but it could wind up being okay. The program would sell whatever permits are sold at the price ceiling (i.e. above the cap) by using the reserve account—and the reserve account is initially stocked with permits from the cap’s pool. In other words, the existence of the reserve account means that there’s a slight tightening of the cap in early years, which means no real cap busting.

If the reserve is depleted then it is re-stocked by selling more offsets to create new permits. And because offsets will almost certainly be cheaper than the ceiling price, subsequent permits sold in excess of the cap will effectively get offset-plus.

There’s more explanation of these features below the jump.

Okay, now let’s dig in.

Emissions targets. The bill tightens the emissions targets a bit beyond the House bill, aiming for a 20 percent reduction below 2005 levels by 2020 and a roughly 83 percent reduction by 2050. If you want more top-level analysis like this, you can find plenty more in the mainstream media coverage. Here (WaPo) and here (NYT), for example. I’m going to concentrate on the more detailed stuff.

Emissions benchmarks. Getting ignored by the media coverage that I’ve seen is that, like the House bill, Kerry-Boxer sets an emissions baseline using an absolute amount of carbon. Normally that might be okay, but it would certainly be better if the bill were to benchmark reductions to actual levels in some year, perhaps 2009 or 2010. That’s because US emissions have dramatically fallen off recently and it might be smart to capitalize on those reductions rather than sticking with somewhat arbitrary numbers based on 2005 emissions.

Timing. The program begins in 2012 for liquid fuels (oil plus a few others), electricity generators, and manufacturers of a few carbon-intense gases. Most stationary industrial sources come into the program in 2014. Local natural gas companies are covered starting in 2016.

Point of regulation. Upstream for oil, at the point where it is introduced into commerce. Upstream for industrial sources, at the plant or smokestack. Upstream for coal- and gas-fired electricity generators, at the plant. Midstream for residential natural gas, at the local distribution company.

Coverage. All seven greenhouse gases, plus a promise to take a look at “black carbon.” Entities are regulated under the cap and trade program when they have annual emissions in excess of 25,000 tons of carbon-dioxide-equivalent. Entities must provide official reporting data above 10,000 tons.

Allocations. [Sound of crickets chirping.] The bill is eerily silent on allocations. It goes to a good deal of trouble to set forth a detailed list of entities and programs that will receive free allowances and programs that will receive auction revenue, but it doesn’t give specific numbers. Presumably, this is going to be left to the Senate Finance committee and other negotiations. There is one exception, however, because the bill appears to mark off fully 25 percent of the allowances for auction with the proceeds going into a deficit reduction account.

Offsets. The bill takes an expansive view of offsets, like the House bill, allowing 2 billion tons of offsets annually. That amounts to about 43 percent of total compliance obligations in the first year of the program — but the percentage grows over time because the total tons of allowable emissions falls while the number of allowable offsets stays fixed. (There are, however, provisions that allow administrative or legislative changes to the number of offsets.) The right to purchase offsets is allocated to regulated entities pro rata using a formula based on historical emissions. The program also allows “term offsets”—i.e. non-permanent offsets—but these must be replaced at the end of their term by additional term offsets, permanent offsets, or emissions permits.

Offset limitations. Of the 2 billion allowable tons, no more than 1.5 billion can be from domestic sources and no more than 500 million can be from international sources. Moreover, international offsets must be retired at a discount rate—1.25 tons of offsets for every 1 ton of carbon-dioxide-equivalent. The discount rate doesn’t kick in until 2018. It is not clear (to me, anyway) if this discount rate effectively lowers the number of tons of emissions that can be replaced by offsets to 400 million (i.e. 500 million tons of offsets, discounted by 1.25, would cover only 400 million tons of CO-2 emissions). There are provisions that allow the number of international offsets to rise to 750,000 tons in the event that there is a shortfall of available domestic offsets. (The escalating international offsets feature has been mischaracterized in the coverage, in part, I’m guessing, because the official bill summary is not clearly worded.) Additional offsets may be used to restock the “market stability reserve,” about which more later.

Market design. The bill allows unlimited banking. It assigns an annual vintage to each permit but allows regulated entities a two year compliance period (which is functionally the same as unlimited borrowing from 1 year into the future). Limited borrowing of up to 15 percent of an entity’s compliance obligation is allowed from 1 to 5 years in the future, but borrowed credits must be repaid with an annual interest rate of 8 percent. (In other words, if today I borrow 1 permit from 2012 then I must repay it by 2012 with 1.24 permits.) There are no restrictions on who can buy, sell, hold, or retire permits. That means banks and brokerages will be allowed; it also means that individuals and nonprofits can purchase permits and retire them. Most of the important market oversight decisions are being left to Senate amendments.

Auction design. Only regulated entities will be allowed to bid. Auctions will be held quarterly using a single-round, sealed-bid, uniform-price format. Smart.

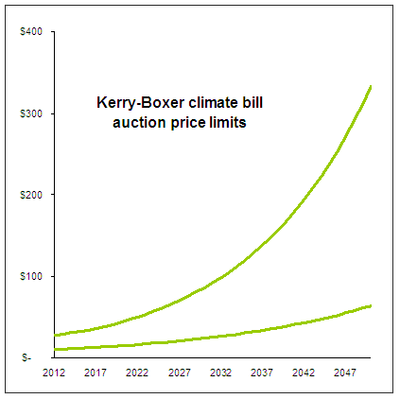

Price floor (aka the reserve price). The bill sets a price floor at $10 for 2012 with the floor rising annually at the rate of inflation plus 5 percent. I haven’t yet seen anyone mention that the $10 is denominated in 2005 constant dollars, which means that the actual nominal floor price will be in excess of $11. (According to the US government’s official inflation calculator, $10 in 2005 dollars is $11.05 in 2009 dollars.)

Price ceiling. The second half, along with the price floor, of what is being called a “price collar,” a term I find incredibly annoying. Additional permits, beyond the limit of the cap, will be available for purchase from the “market stability reserve” at the ceiling price of $28 in 2012. (But like the price floor, this figure is denominated in 2005 constant dollars, which means that the actual nominal figure will be somewhere north of $31, the current value of $28 in 2005 dollars.) The ceiling price rises annually at the rate of inflation plus 5 percent until 2017; starting in 2018, the annual ceiling price will rise at the rate of inflation plus 7 percent.

Market stability reserve. Though I can’t for the life of me figure out exactly how the stability reserve is initially stocked with emissions permits—apart from some vague language that the program administrator will take it from the pool of permits allowed under the initial cap –it is re-stocked by selling additional offsets, which are converted into permits for the reserve. (It is not clear whether these additional offsets, if they are international, are subject to the 1.25 to 1 discount rate that applies to offsets used for ordinary compliance.) The reserve also collects any unsold permits from previous auctions, as might happen if the auction hit the price floor. There are limits on how many permits can be released at any one time from the reserve—15 percent more than the cap until 2016; 25 percent more than the cap from 2017 on; and never more than 25 percent of the total permits in the reserve –which, of course, effectively makes for a limit on the number of permits that can be sold at the price ceiling. (It seems that this limitation, together with a fixed price point for the permits, might create market distortions in the event that actual demand for permits far outstripped the total number of available permits.) In summary: the market stability reserve makes the price ceiling no more problematic than the quality of the program’s offsets.

Miscellaneous good stuff. The bill does not preempt EPA authority under the Clean Air Act to limit climate pollution from stationary sources as the House bill did. It also provides compensation for cap and trade credits issued by California, RGGI, or the Western Climate Initiative. And it appears to include stronger provisions for assisting international adaptation and low-carbon development, though I’m murky on the details. Finally, the bill appears to tighten up the regulations for covering biomass, biofuels (and biofuels accounting), and it declines to put USDA in charge of agricultural offsets.

Miscellaneous annoying stuff. The bill does not cover fugitive methane emissions from mines, pipelines, etc., but rather allows these sources to qualify as offsets. That means that there will be more offsets available than under the rules in Waxman-Markey. There’s also a ton of stuff about nuclear power and clean coal, but I haven’t waded through the particulars.

Miscellaneous-miscellaneous stuff. The bill distributes “compensatory allowances” for permanent carbon capture and sequestration, as well as for non-emissive use of fossil products. There are some provisions for a border adjustment on carbon-intensive trade goods. There is a semi-separate program designed to ramp down the consumption of perflourocarbons.

Terminology. Interestingly, the term “cap and trade” has disappeared from the bill. (Must not poll well or something?) Rest assured that the policy is still there, though the cap and trade program is now referred to as “pollution reduction and investment.” And unlike the House bill which goes by the name ACES, the Senate’s Clean Energy Jobs and American Power Act doesn’t have a zippy/dorky acronym. For some reason, CEJAPA just doesn’t roll off my tongue. But who cares, right?

Non cap and trade stuff. Like the House bill, the Kerry-Boxer bill has a ton of other stuff in it: green jobs, renewable energy, energy efficiency, clean coal, research and development, and so on. I’m not touching this stuff for now. (Sorry folks, it’s 821 pages long and I’m in triage mode.) One interesting criticism of the bill’s weakness on energy efficiency is here.

Last updated at 1:50 p.m. on October 1.

***

The official bill is here (big pdf). Various summaries (and a link to the bill) are here. I’ve appreciated this summary by Jesse Jenkins at The Energy Collective; it’s always smart to check in with Joe Romm over at Climate Progress; and Brad Plumer has an intelligent summary and analysis at The New Republic. Plus, Grist has links to a wide range of reactions.

Keith Beatty

The atmospheric greenhouse effect, an idea that many authors trace back to the traditional works of Fourier (1824), Tyndall (1861), and Arrhenius (1896), and which is still supported in global climatology, essentially describes a ï¬ctitious mechanism, in which a planetary atmosphere acts as a heat pump driven by an environment that is radiatively interacting with but radiatively equilibrated to the atmospheric system. According to the second law of thermodynamics such a planetary machine can never exist. Nevertheless, in almost all texts of global climatology and in a widespread secondary literature it is taken for granted that such mechanism is real and stands on a ï¬rm scientiï¬c foundation. In this paper the popular conjecture is analyzed and the underlying physical principles are clariï¬ed. By showing that (a) there are no common physical laws between the warming phenomenon in glass houses and the ï¬ctitious atmospheric green- house effects, (b) there are no calculations to determine an average surface temperature of a planet, (c) the frequently mentioned difference of 33 â—¦ C is a meaningless number calculated wrongly, (d) the formulas of cavity radiation are used inappropriately, (e) the assumption of a radiative balance is unphysical, (f ) thermal conductivity and friction must not be set to zero, the atmospheric greenhouse conjecture is falsiï¬ed. http://arxiv.org/pdf/0707.1161v4“It is not reasonable to conclude that there is any endangerment from changes in greenhouse gas levels based on the satellite record”National Center for Environmental Economics.http://cei.org/cei_files/fm/active/0/DOC062509-004.pdfProfessor Lindzen proves the effect of CO2 on temperature is a non event.NO LONGER can it be credibly argued that “globalwarming” is worse than previously thought. No longer can it be argued that “global warming” was, is, or will be any sort of global crisis. Recent papers in the peer-reviewed literature,combined with streams of data from satellites and thermometers, now provide a complete picture of why it is that the UN’s climatepanel, the worldwide political class, and other “global warming” profiteers are wrong in their assumption that the enterprises ofhumankind will disastrously warm the Earth.The global surface temperature record, which we update and publish every month, has shown no statistically-significant “global warming”for almost 15 years. Statistically-significant global cooling has now persisted for very nearly eight years. Even a strong el Nino—expected in the coming months—will be unlikely to reverse the cooling trend.More significantly, the ARGO bathythermographs deployed throughout the world’s oceans since 2003 show that the top 400 fathoms of the oceans, where it is agreed between all parties that at least 80% of all heat caused by manmade “global warming” must accumulate, have been cooling over the past six years. That nowprolonged ocean cooling is fatal to the “official” theory that “global warming” will happen on anything other than a minute scale.Not only in the oceans but also in the tropical upper atmosphere, realworld measurements are showing up the scaremongers’ computermodels as useless. All of the models predict that at altitude in the tropics “global warming” should have happened at thrice the surface rate. But half a century of measurement has shown that that warming has not happened either. That, too, is fatal to the “official” notion.

PieChart

Hopefully we won’t make the ridiculous mistake of holding televised “town halls” to “discuss” this bill. “Town halls” maybe. Televised? Stupid.

Gene Thomas

HR3200 REVISITED…… GREEN ENERGY FUNDWe don’t need Allocation Allotments, Carbon Credits or Offsets. They don’t reduce pollution. We need a system that will demand reduction of emissions in addition to furnishing money for a Green Energy Fund.Every polluter will pay an annual Pollution Fee equal to (5%) five percent of the annual cost of the fossil fuel used. The average price of fossil fuel used to generate 65 terra watts in 2008 was 2.402 cents per kwhr .The Fee from power plants, vehicles etc. will add Trillions of Dollars to the Green Energy Fund.Power plants and others using fossil fuel that have not incorporated the most efficient filtering systems will pay a (6%) six percent Fee. Power plants that do not or cannot decrease their emissions will find their Fee increased by (1%) one percent each year. Government backed loans will be available to finance updating the plants to enable a reduction in emissions.Automobiles, trucks, construction equipment and other vehicles including trains that use fossil fuel will be phased into the program and pay the same five percent Fee as above.The Fee for gasoline will be about 13 to 16 cents per gallon* paid on approximately138 trillion gallons annually.Oil wells, gas wells and refineries under construction and in production will pay a Pollution Fee based on another standard to be determined.Price controls will protect the consumers of electric power, gasoline and diesel. Prices increases on electric power will be limited to (5%) five percent per year.NOW IS THE TIME: Before joining with the international Carbon Credit Fiasco.Gene Thomas*Variable with market price.**Ask the DOE for detailed calculations. They have data and experience to provide an accurate confirmation.***Other fuels will have different cost per kilowatt-hour.