As Eric mentions below, Goldman Sachs just sold its interest in the Gateway Pacific coal export project to a Mexican billionaire. It’s far too soon to say what this development will mean for Gateway’s prospects. But when coupled with Ambre’s difficulties finding new financing, Goldman’s move underscores an important new reality: Wall Street now views Northwest coal exports as too risky to touch.

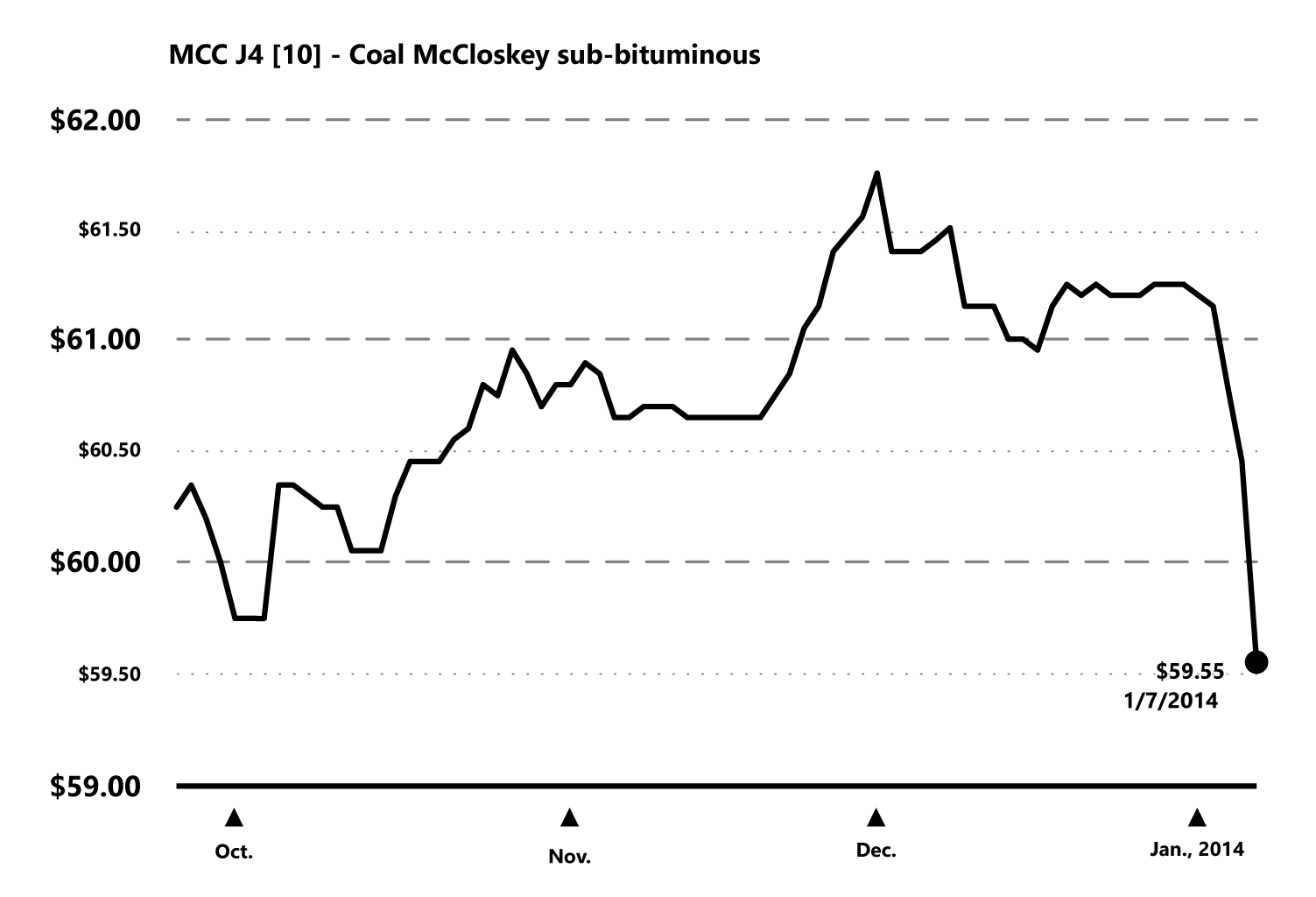

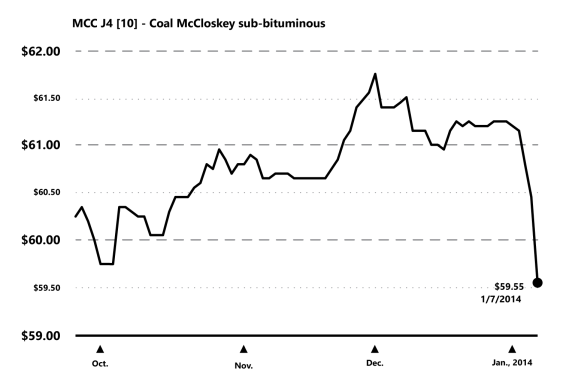

And for good reason. Pacific Rim coal prices have taken a severe beating over the past few years, with prices for benchmark Australian coal falling from more than $132/ton in early 2011 to less than $78/ton in September 2013. And after clawing back a few dollars late last fall, Pacific Rim coal has been caught in yet another sell-off over the past week, as shown in this chart of Indonesian sub-bituminous coal futures…

So it could be that Goldman got out of the coal export business just in time. Of course, they had plenty of warning: Wall Street analysts have been issuing increasingly dire assessments of coal export prospects for more than a year. Take a look:

- November 2012, Bank of America Merrill Lynch, 2013 Energy Outlook. “We see a downward path for global coal prices…Seaborne thermal coal continues to battle with heavy physical oversupply as producers still export too much into a weak seaborne market …Inventories are bloated as demand just cannot keep up.”

- February 2013. IHS CERA, Coal Rush: The Future of China’s Coal Market. “[I]nternational suppliers may find themselves in a much tougher market as they face competitors that previously did not exist. The major Indonesian suppliers will always compete effectively in southern China…but mines elsewhere in the world will struggle to find a competitive edge.”

- May 2013. Deutsche Bank, Commodities Special Report, Thermal Coal: Coal At A Crossroads. (No URL, but summarized here.) “[N]ew demand preferences in the largest consuming nations will result in much lower demand growth going forward, pushing prices lower in real terms through 2020.”

- June 2013. BernsteinResearch, Asian Coal & Power: Less, Less, Less…The Beginning of the End of Coal. (No URL, but summarized here.) “Regional miners will see almost zero demand in China from 2015…Once Chinese coal demand starts to fall, there is no robust growth market for seaborne thermal coal anywhere.”

- July 2013. Goldman Sachs Rocks & Ores, The window for thermal coal investment is closing. “Earning a return on incremental investment in thermal coal mining and infrastructure capacity is becoming increasingly difficult…[T]hermal coal is a geologically abundant resource in an industry with relatively low barriers to entry. As coal demand becomes increasingly constrained, the competition among suppliers is likely to intensify.”

- September 2013. Citi, The Unimaginable: Peak Coal in China. “[S]ignificant shifts in China’s economy and power sector are now under way that demand a reassessment of Chinese coal’s perpetual climb…The same macro forces that are driving the economic transition and lowering power demand should also sharply decelerate coal’s use.”

The Goldman-managed infrastructure fund that sold its stake in Gateway originally had been marketed to risk-averse investors, such as pension funds—the sort of folks who expect stable returns without big ups and downs.

So the fact that Gateway’s new owner is a high-flying international billionaire suggests that the transition in Wall Street’s perception of coal exports is now complete. Wall Street used to view Northwest coal exports as a blue chip investment. But the new view—backed not just with words but with money—is that they’re in territory reserved for risk-hungry financial speculators.

Yo

Can it be that we are now seeing the end of the export of raw materials and the beginning value added exports. We need more value added exports in the timber industry. Meteric squares shipped to the orient were all the rage and provided jobs. Time to re-think our love of thowing people away as to expensive to employ.

We, in the Vancouver, BC area, seem to be bucking these coal trends. Planned and proposed coal export terminal expansions are still being pushed by the BC government, coal mines, and transport industry. Seems as Oregon and Washington stop coal exporting, it is moving north of the border. Any help is appreciated in how to close the BC shoreline to coal exports. Everyone loses if this coal is sent to China, Korea, or wherever.