It’s earnings season on Wall Street, and Cloud Peak Energy—one of the biggest coal producers in the Powder River Basin—just released its first-quarter results. By coal industry standards, it was good news. Stock analysts had expected the company to lose 12 cents per share for the quarter, but the company’s financial statements revealed losses of only 5 cents per share, which led to a modest rally in Cloud Peak’s otherwise disappointing stock prices.

You know things are bad for the coal industry when a multi-million dollar loss counts as a positive development.

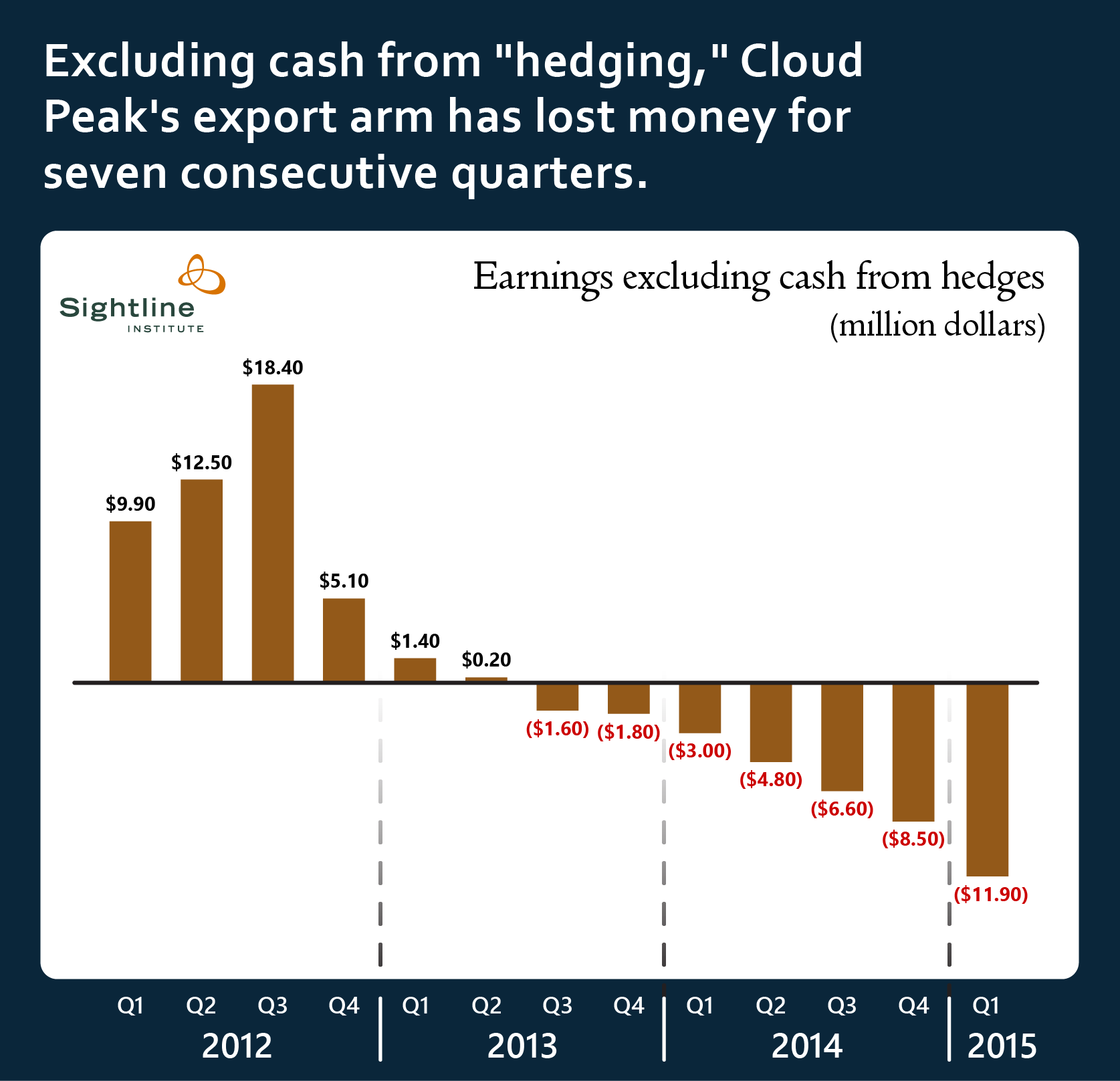

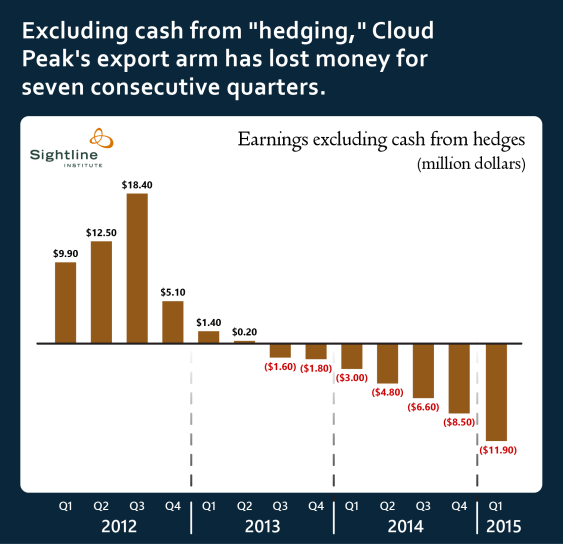

But Cloud Peak’s financial statements also show a trend that must be troubling to the company’s investors: the firm’s coal exports to Asia are hemorrhaging red ink.

As the above chart shows, the company’s export division has been losing money on export sales since the middle of 2013.

But two recent changes to Cloud Peak’s export business deepened the company’s export losses in the first three months of this year.

[prettyquote align=right]Cloud Peak’s #coal exports to Asia are hemorrhaging red ink.[/prettyquote]

First, Cloud Peak has ramped up its export volumes. Last summer, Cloud Peak signed long-term contracts to boost the company’s exports through the Westshore coal terminal in southwestern British Columbia. At the time, Cloud Peak crowed about getting port space on the cheap. But so far it has been an expensive purchase: international coal prices have fallen so low that the company now loses about $8 for every ton of coal it ships overseas. So for the foreseeable future, higher export volumes will lead to steeper losses.

Second, the steps that Cloud Peak took to protect itself against falling coal prices are coming to an end. Back in 2011 and 2012, when international coal prices were high, Cloud Peak locked in futures market “hedging” contracts that virtually guaranteed profits even if coal prices fell. From mid-2013 through late 2014, the gains from those hedges allowed the company’s export arm to claim a profit, even though they were losing money on actual coal sales. But those hedge positions are now running thin, and will be completely exhausted by the end of 2016. If the futures market is any guide to coal prices over the coming years, this means that the losses from Cloud Peak’s export arm will continue throughout 2015, and then deepen in 2016 and beyond.

In short, Cloud Peak’s gamble on Asian exports is looking more and more like a bad bet. The once-exuberant Pacific Rim coal market is in the doldrums, and looks poised to stay there. And the losses that Cloud Peak is now sustaining on its export strategy are weighing heavily on the company’s bottom line.

You call your campaign Honest Elections. But you

can be Honest. Your paid signature gather’s r not

wearing badges or dont have signs on their tables.

Thats being dis Honest to the Voters.

Maybe U should have a badge say which special interest

is paying for the Signatures.