Rebecca Solnit describes how democracy can be captured by Tyranny of the Minority—the small group that thinks it knows best and tries to exclude the masses.

Vox has an interesting take on left-wing economics and right-wing populism in Europe and the United States: countries with the most robust social safety nets might also have the strongest far-right movements.

The key point here is not that people are irrational; it’s that this irrationality comes from a very rational place. People fail to distinguish what they know from what others know because it is often impossible to draw sharp boundaries between what knowledge resides in our heads and what resides elsewhere.

This is especially true of divisive political issues. Your mind cannot master and retain sufficiently detailed knowledge about many of them. You must rely on your community. But if you are not aware that you are piggybacking on the knowledge of others, it can lead to hubris.

Also at the New York Times, Nicholas Kristof writes about new research showing a truly precipitous decline in sperm quality and male fertility. There’s good evidence that the culprit is chemical endocrine disruptors, which are loaded up in the plastics, cosmetics, couches, pesticides and countless other products we use every day.

On Tuesday, Sightline senior research associate Tarika Powell joined KBAI’s Joe Teehan to discuss her latest report detailing the 20 liquefied natural gas projects proposed for the shores of British Columbia. The projects would stretch from the Salish Sea in the south to Stewart, BC, in the north, with major hubs at Kitimat and Prince Rupert. The province’s LNG ambitions could make it the world’s largest LNG exporter.* Listen in below (from 2:30 to 19:35), or find the full program online here.

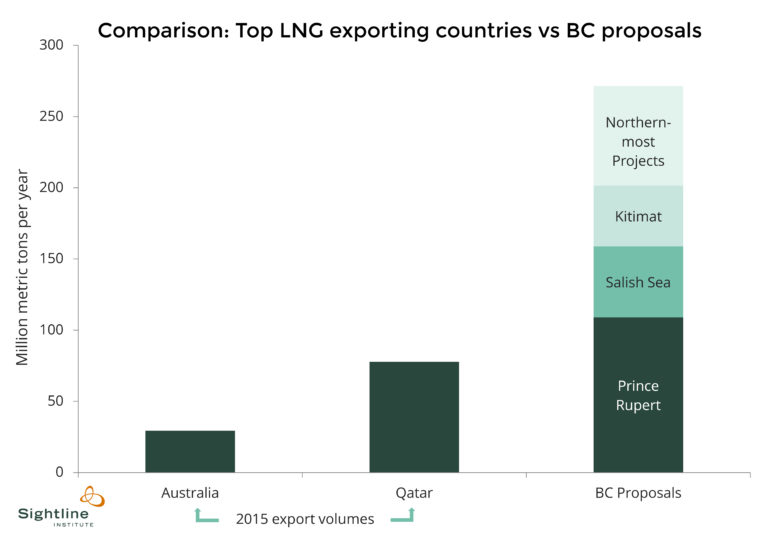

BC Wants to Produce Four Times as Much LNG as World’s Largest Exporter

Even now that Shell hasannounced its decision to discontinue further development on the Prince Rupert LNG project, there are still nineteenLNG export proposals pending in British Columbia. Five of the proposals are on the Salish Sea, four are clustered at Kitimat, six near Prince Rupert, and another four are proposed north of Prince Rupert. While the sheer number of proposals is striking (Washington and Oregon combined have seen only four LNG proposals in the last decade), the combined production capacity of the proposals is stunning.

If the nineteen proposals were to go forward, the province would become the world’s largest LNG exporter—by a long shot. According to the International Gas Union’s2016 World LNG Report, the top LNG-exporting countries are Qatar and Australia. Qatar, which is located on the Persian Gulf near Saudi Arabia, has been the world’s largest LNG exporter for a decade. Producing 78 million metric tons of LNG, Qatar claimed about 32 percent of the global LNG market share in 2015. Australia produced the second largest global market share at 12 percent, exporting 29.4 million metric tons of LNG in 2015.

The planned production capacity of BC’s LNG proposals dwarfs the world’s top LNG exporters.

Original Sightline Institute graphic, available under our free use policy.

In aggregate, the LNG proposals in BC would produce more than 270 million metric tons of LNG per year, three-and-a-half times the volume exported from Qatar and nine times the volume exported by Australia. In fact, the production capacity of the BC proposals rivals that of all the LNG production capacity in the world in 2015, which was 301.5 million metric tons.

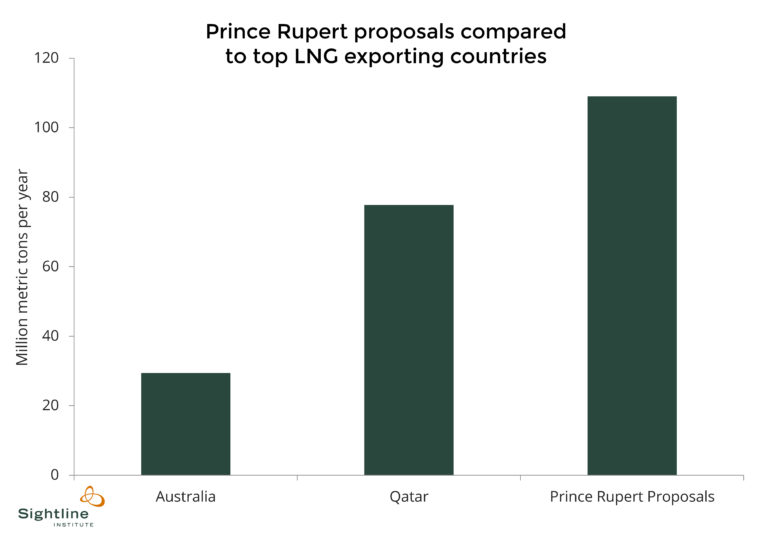

Even if only the projects proposed for the Prince Rupert area advanced, BC would still produce 109 million metric tons of LNG—slightly more than world leaders Qatar and Australia combined.

Original Sightline Institute graphic, available under our free use policy.

The provincial government hopes to havethree plants in operation by 2020—a rather ambitious expectation given that none of the projects has actually begun construction and that experts estimate it takesabout five years to build large export facilities like these. Plus, there are any number ofunfavorable conditions in the LNG market, making itdifficult for the project backers to secure the long-term contracts necessary for their financing. While no one expects all nineteen remaining projects to move forward, it’s worth understanding the province’s ambitions in the context of world LNG exports—they are truly titanic.

Note and methods: Data for LNG production volumes in BC are drawn from multiple sources that are cited extensively in Sightline’s March 2017 report on the industry,Mapping BC’s LNG Proposals. Since one of the projects (Nisga’a LNG) has not applied for an export permit,its export capacity is not known. This analysis includes 18 of the 19 remaining proposals.

BC’s ‘Wild West of Political Cash’ Fuels a Fossil Fuel Frenzy

Unusual for any modern democracy, the province actually has no limit on contributions to political parties. There are no caps on checks from individuals, corporations, or even foreign entities doing business there or working directly with the government. (By contrast,charitable organizations, including NGOs, are barred from making political donations.) In fact, the premier is actually awarded a special stipend from the party—over and above the government salary that comes with the office—that is funded directly by political contributions.

The dirty energy development schemes are not divorced from politics.

As the CCPA report shows, lightly regulated political giving is an issue that seems pronounced with the fossil fuel industry—the coal, oil, and gas companies that have designs on converting BC into a global superpower of carbon pollution-based exports. The province is already a major producer of coal (mostly high-grade coal for steelmaking) and fracked gas. And in recent years the fossil fuel industry has proposed two new major oil pipelines to carry tar sands, four new or expanded coal terminals, at least six new gas pipelines, and no fewer than twenty liquefied natural gas (LNG) facilities on the coast, some of which would be the biggest in the world.

The dirty energy development schemes are not divorced from politics. Examining giving to the province’s two leading parties, the right-leaning Liberal Party and the left-leaning NDP, the report finds that “48 fossil fuel companies and industry groups donated $5.2 million over the eight-year period between 2008 and 2015. Of this total, 92% went to the BC Liberal Party.” (Nota bene for American readers: the BC Liberal Party is the province’s governing center-right party and unaffiliated with the national Liberal Party of Prime Minister Trudeau.) The vast majority of that money—about three-quarters of it—came fromjust ten contributors. And of those ten contributors, only two are actually headquartered in the province: half are based in Calgary (sometimes thought of as the Houston of Canada for its central role in the oil industry), while three more are either based in the US or are subsidiaries of US companies.

The report also provides the first comprehensive look at fossil fuel industry lobbying in the province, identifying 19,571 contacts between government officials and lobbyists from just ten firms between April 2010 and October 2016—that’s an average of 14 contacts per day. By contrast, the entire array ofenvironmental NGOs in the province had just 1,324 lobbying contacts over the same period.

Still, as infused with dirty energy money as BC politics may appear to be, it may actually be a less severe problem than it is in the US. As Sightline has documented in previous work on democracy issues,Canadian elections are generally less influenced by money than they are in the United States. That seems to be true even when comparing British Columbia and the Northwest states of Oregon and Washington, which are roughly similarly sized. Examining political spending for just two years, 2013 and 2014, Sightline documented fossil fuel industry political spending of more than $3 million in Washington and $2 million in Oregon. A related analysis by Oil Check Northwest tallied coal, oil, and gas industry political spending of nearly $8 million in Oregon and more than $12 million in Washington over the six-year period from 2009 to 2014. (To be clear, CCPA’s accounting in British Columbia, which focuses on giving to parties, is not directly comparable to Sightline’s or Oil Check’s methodologies, which count lobbying expenditures and contributions to political action committees, as well direct contributions to candidates and parties.)

Although political spending looks to be higher in the Northwest states, the fossil fuel industry’s campaign cash does appear to be having more success in British Columbia. The executive branches in Oregon and Washington have largely cast a skeptical eye on dirty energy proposals, but the government of British Columbia is actively cheerleading LNG development and coal exports, while offering only modulated concerns over new oil shipment projects. In that context, the CCPA report is a timely warning that the success ofthe Thin Green Line—the Northwest’s regionwide resistance to carbon pollution-based exports—may be available for purchase from British Columbia’s political leaders.

Seattle’s Flawed Plan for Mandatory Housing Affordability Would Suppress ‘Missing Middle’ Housing

This article is part of a series on Seattle’s proposed Mandatory Housing Affordability (MHA) program. Previously, I identified inconsistencies in the proposal and presented case studies (here and here) on two key housing types. In both cases, MHA would suppress homebuilding and backfire on the city’s affordability goals. Next up: apartments in MHA’s low-rise upzones.

In Seattle urban planner-speak, “low-rise” means modest-scale multi-family housing such as townhouses, rowhouses, and small—3 or 4 story—apartment buildings. These homes fill the gap between single-family houses and large-scale apartments, providing much needed affordable home options in city neighborhoods near schools, transit, and jobs. They are often referred to as “missing middle” because in many US cities the predominance of single-family zoning has made them uncommon.

Seattle’s proposed Mandatory Housing Affordability(MHA) program would allow the developers of low-rise buildings to construct larger structures with more homes in them. And it would require that in exchange, they either provide a quota of subsidized affordable homes within the building or pay a fee to the city, with which Seattle would subsidize homes elsewhere. The theory of MHA is sound, but implementation is risky: if the mandate costs homebuilders more than the added apartments let them earn, they may choose not to build at all, yielding neither additional market-rate nor affordable housing choices. A policy intended to be a win-win becomes a lose-lose.

Indeed, my previous case studies of mid-rise and high-rise upzones found that MHA as proposed —and now implemented in the University District—is so poorly balanced that it would slash builders’ return on investment and suppress homebuilding. Disappointingly, it’s a similar story for the low-rise apartments I analyze here: the draft low-rise MHA policy is imbalanced and will slow construction and produce less housing—subsidized and market-rate—as a consequence. And less housing means more competition for what’s available, rising rents, and more displacement of low-income families and individuals.

MHA’s financial hit on low-rise homebuilding would be less severe than what my previous analysis indicated for mid-rise and high-rise examples. But most low-rise housing is built by small businesses that have less tolerance for added costs than the larger companies that build mid- and high-rise apartments. MHA as currently proposed would not only undermine Seattle’s goals to build more affordable homes for low-income residents, but also the city’s goals to create a full spectrum of housing choices for all.

The good news is that Seattle officials can fix it. The city could grant more capacity in the MHA upzone along with complementary changes to development rules to ensure builders can make use of that extra capacity. Or they could make the affordability requirements less demanding. Or they could combine those options. Either way, bringing MHA into balance will unlock its potential to deliver Seattle neighborhoods more subsidized homes and more market-rate missing middle housing.

Four-story apartment on 16th and Denny in Seattle, by Dan Bertolet, used with permission.

Assessing MHA’s net effect on affordability

In a previous article I described the rationale behind my method of assessing MHA. Here’s a synopsis for newcomers; skip ahead if you don’t need it:

The root cause of Seattle’s soaring housing prices, leading to displacement, monster commutes, and community disruptions, is a shortage of housing; to keep prices down for everybody, we need more homes of all kinds. Building market-rate homes is good for affordability.

Regulations that hold back the production of market-rate housing ultimately hurt the city’s lowest income individuals and families most through the housing market’s cruel version of musical chairs that results in fierce competition for what’s available in the city and leaves no homes for those with the least to pay for them.

MHA’s net impact on affordability depends not only how many subsidized homes it creates but also on how it affects market-rate production. If, for every one subsidized home created, the policy also prevents the production of two market-rate homes, the outcome will be a net loss of affordability.

The rate of private housing development is determined by risk versus return. When regulations make homebuilding more expensive or risky, less housing gets built.

The hinderance on homebuilding caused by MHA’s cost is not nullified by reduced land prices because when owners get offered less for property that is producing income, they will be less likely to sell it, and if they don’t, no new housing gets built.

Designing and assessing MHA requires a comparison of homebuilding feasibility under existing regulations versus under the proposed MHA requirements. Inexplicably, the City of Seattle has not conducted this type of before-and-after analysis of MHA and does not account for feasibility—that is, the market test—in its MHA production projections.

Feasibility analysis is highly sensitive to assumptions about rent, construction cost, capitalization rates, and other factors. But before-and-after analysis is largely immune to the noise caused by imprecise assumptions: they largely cancel out to reveal the most critical result which is the change in feasibility caused by MHA.

Feasibility does not operate like a light switch, contrary to what is presumed in the City’s MHA feasibility study and other similar analyses (here and here, for example). Just because the costs imposed by MHA don’t drop the return on investment (ROI) below some arbitrarily chosen cutoff doesn’t mean it’s not harming feasibility. Across the city, on average, feasibility is a game of probabilities: like any other building regulation, the more MHA drives ROI down, the less new housing becomes available to city residents

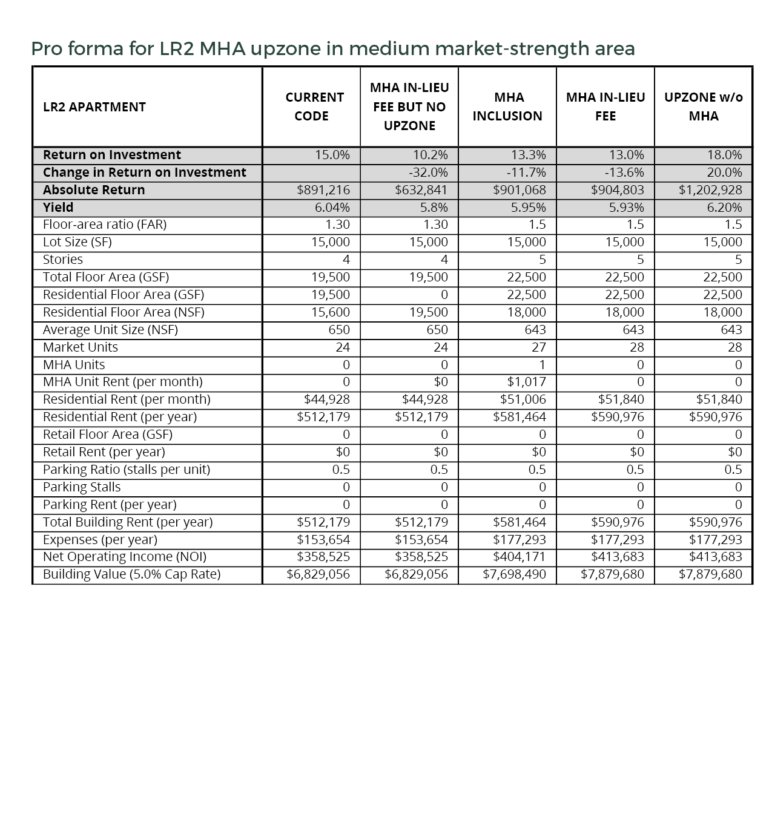

Case study: LR2 and LR3

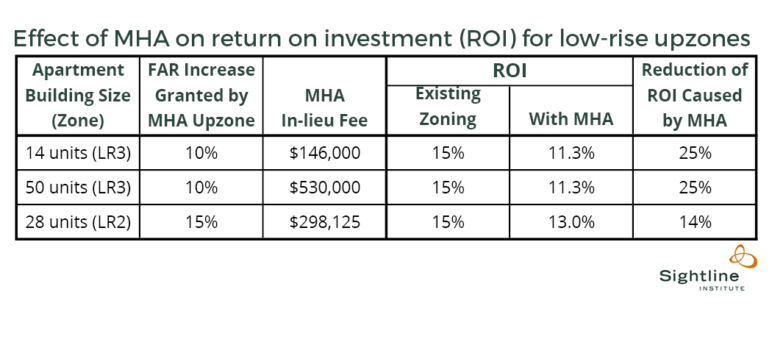

I assessed three small apartment building prototypes from the city’s own analyses to illustrate likely development under the proposed MHA low-rise upzones (details here, here, and here). Following the before-and-after method I described previously, I applied static pro formas to estimate how the MHA upzone would change the homebuilder’s return on investment (ROI) compared to a baseline project under existing zoning that would deliver a 15 percent ROI.

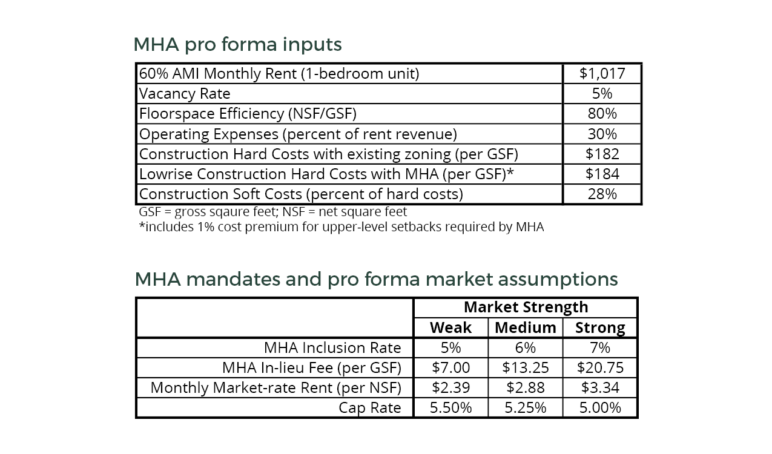

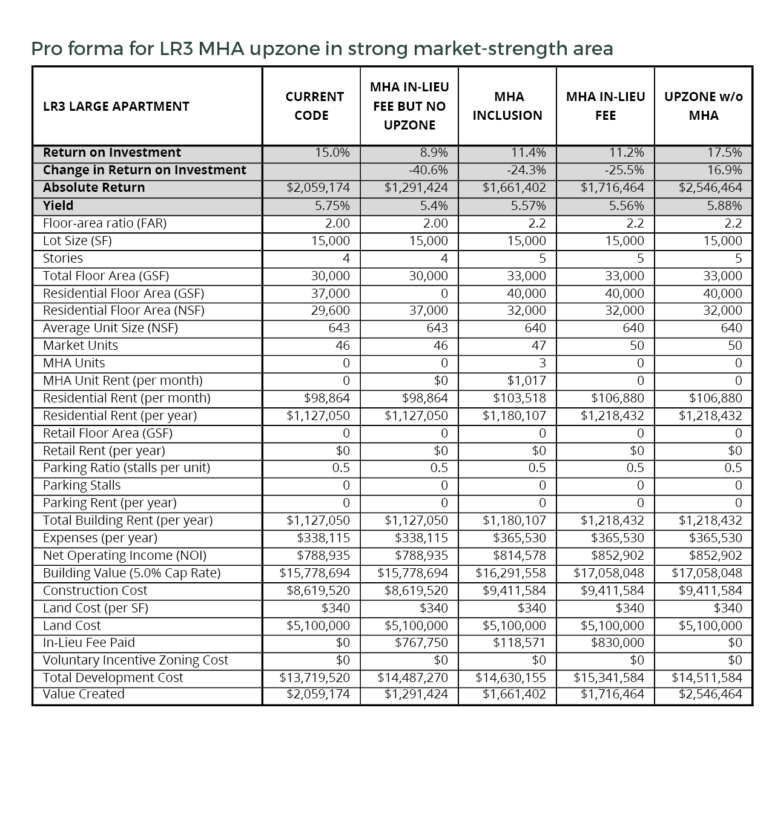

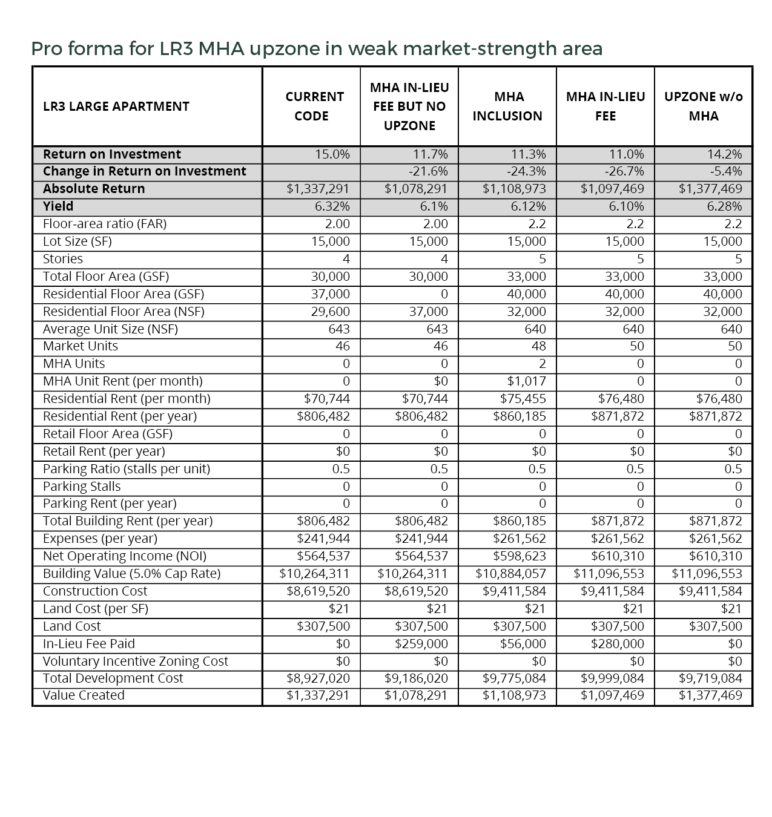

I focus on results under the assumptions for a medium market-strength area in Seattle because that is where these projects would most likely be built. (Results for low and high market-strength areas are qualitatively similar and are in the appendix). The proposed MHA performance (inclusion) and payment (in-lieu fee) amounts are 6 percent subsidized units or $13.25 per square foot of building, respectively. Because these prototypes have relatively small numbers of units, setting aside 6 percent of them will sometimes be mathematically impossible. Many developers will have no option but pay the fee, so this article highlights results for the in-lieu fee option. (Results for inclusion are similar and are in the appendix)

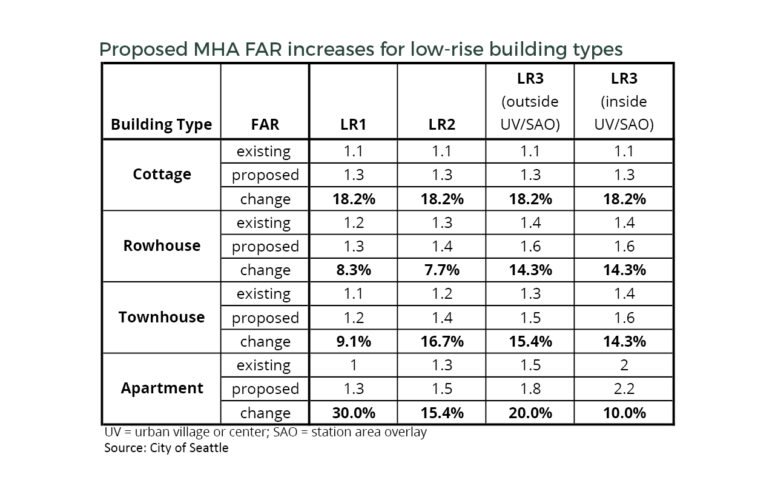

I chose three examples that cover a range of sizes and included examples in both the low-rise 2 (LR2) and low-rise 3 (LR3) zones to illustrate the effect of the increase in allowed floor-area-ratio (FAR) granted by the upzones. (For reference, a table of all the proposed MHA low-rise upzones is in the appendix.) For both the LR2 and LR3 upzones, planners have proposed a requirement for 12-foot upper-level setbacks on the top floor. Because this requirement introduces construction inefficiencies, I assume a 1 percent construction cost premium.

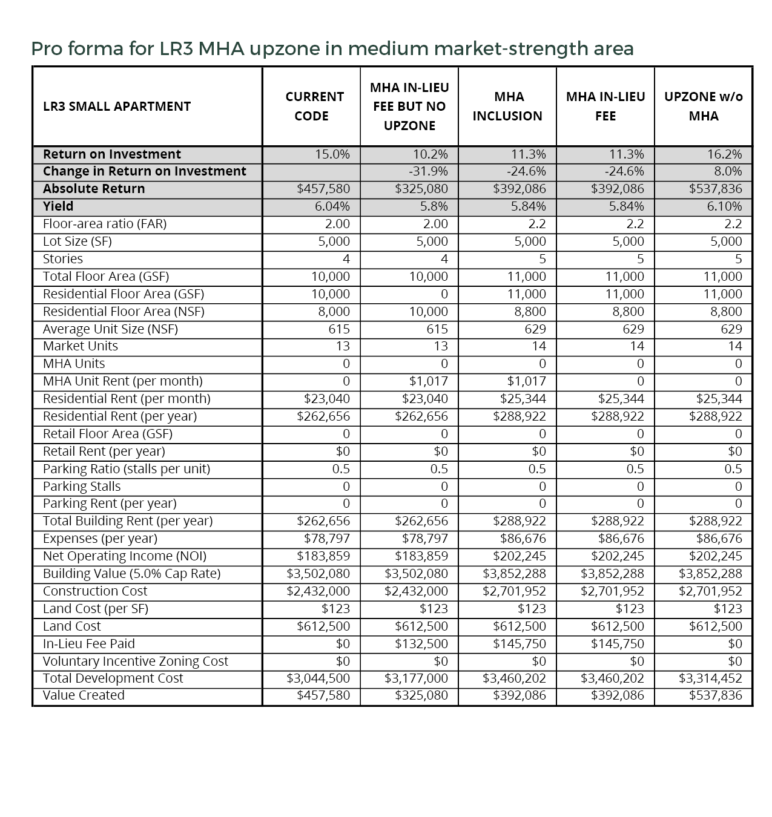

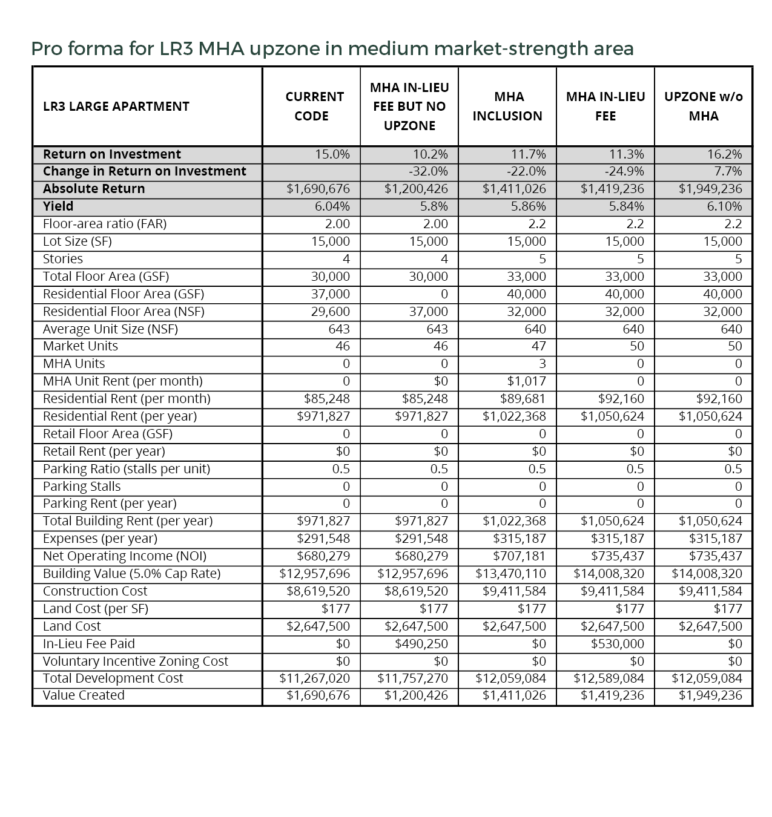

The table above shows the pro forma results. For the two LR3 prototypes, the MHA upzone knocks down ROI by one quarter. For the LR2 prototype, the ROI loss is 14 percent. The simple reason LR2 looks better: the LR2 upzone grants more capacity (more FAR), and that allows the developer to add a larger share of market-rate units, which offsets more of what the developer is required to pay in fees.

These ROI reductions for low-rise apartments are smaller than my previous analysis found for MHA’s proposed mid-rise and high-rise upzones. That’s mainly because for low-rise, enlarging a building to conform to the MHA upzone does not require a switch to more expensive construction. Builders simply add another floor of the same wood-frame construction.

I did not analyze the proposed MHA upzone for LR1, because it would typically involve a major change in building type. Instead of homes for sale, the upzone would likely result in apartments for rent—a change that greatly complicates the value comparison. To encourage small apartments, the proposed LR1 upzone removes the existing limit on numbers of apartments and exempts from FAR any apartments that are partially below grade, although it also adds a requirement for family-sized units. My preliminary estimates suggest that the proposed upzone’s generous FAR boost of 30 percent would likely balance the MHA mandates and fees. ROI would likely stay about the same, an MHA upzone done right. It might even improve ROI compared to existing zoning. But historically, production of new homes in LR1 zones has lagged behind production in LR2 and LR3 zones. So the LR2 and LR3 zones matter more to Seattle’s housing future.

Three-story condo building at 16th and Pike in Seattle, by Dan Bertolet, used with permission.

What’s at stake

The estimated reductions in ROI shown above for the LR2 and LR3 zones will result in less low-rise homebuilding under MHA as proposed, compared to homebuilding that would occur under existing zoning. Unfortunately, there is no easy way to quantify the new homes sacrificed. To give a better sense of what’s at stake citywide, from 2006 to 2016 low-rise comprised 19 percent of all homes built in Seattle. For comparison, Seattle’s neighborhood commercial (NC) zones—the zones where all the new four- and six-story mixed-use apartments are built—accounted for 21 percent.

As noted above, the estimated drops in ROI caused by MHA are not catastrophic, especially in the case of LR2. However, compared to larger-scale mid-rise and high-rise developments, low-rise homebuilding is more likely to be more susceptible to death by reduced returns. Because low-rise buildings are relatively modest in size and cost, they are most often developed by local, small-scale homebuilders who are more vulnerable to added expenses. Larger projects usually have the benefit of financial backing from deep-pocketed institutional investors who have access to lower cost capital and can accept lower returns if necessary. In contrast, small-scale local developers are typically faced with less favorable lending terms, and they may be literally risking everything they own on a project.

Implementing MHA without tuning it for feasibility is a recipe for failure—not just for HALA’s promises but for the very people that HALA promises to protect.

Consider the prospect of building the small LR3 apartment prototype. Today, by my pro forma estimates, investors would weigh the risk of a $3.2 million total investment against a potential return of $474,000. After MHA, they would weigh the risk of a larger $3.6 million investment against a smaller return of $422,000. In addition, the developer would have to write a check up front to the city for $146,000 before even receiving a permit to start construction.

Would the loss of incentive caused by MHA stop all low-rise apartment projects? No. But neither would it be harmless. The shrinking returns and rising costs would stifle projects. And every new home sacrificed matters, because one less home means one more low-income household pushed out of Seattle. Every time a homebuilding project that would have occurred under current zoning gets shelved because of MHA, the housing shortage gets worse and stiffened competition for the homes we have forces families without resources out. Implementing MHA without carefully tuning it for feasibility is a recipe for failure—not just for the goals of Seattle’s Housing Affordability and Livability Agenda (HALA), but for the very people that HALA promises to protect.

How to fix it

To balance the scales, Seattle can either increase the value of the upzones or reduce the affordability requirements.

Allowing a higher FAR—a larger building—is the most straightforward means. In particular, the proposed LR3 FAR boost of only 10 percent is low compared to almost all of the other proposed MHA upzones. For the larger LR3 prototype, raising the FAR boost to 25 percent would increase the estimated ROI to 13.7 percent, getting closer to the 15 percent ROI baseline. For the LR2 prototype, raising the FAR boost to 25 percent would increase ROI to 14.8 percent.

As shown in the FAR table in the appendix, the proposed MHA upzone for apartment buildings in LR3 zones not located inside a designated Urban Village or Station Area Overlay grants a 20 percent FAR boost. The feasibility of homebuilding projects in these specific areas would suffer less under MHA than the LR3 prototypes I analyzed, but this FAR discrepancy again illustrates the troubling inconsistencies in the MHA proposal.

For typical low-rise buildings, however, the floor space that can be built is often more constrained by other rules than by FAR. Seattle’s code, for example, currently requires larger side and rear setbacks for apartments than for townhouses and rowhouses. The code also erodes design efficiency by mandating a maximum “façade length,” that is, the uninterrupted length of a building’s exterior walls. Seattle’s HALA called out the need to revise these standards (recommendation MF.6):

In some of the low-rise multifamily zones, townhouse or rowhouse forms of development are favored by the code over stacked flats (apartments or condominiums located on different levels in a building). This can limit production of potentially greater numbers of housing units, or limit the housing product to ownership units instead of rental units. The City should change the code to allow more stacked flats in all low-rise zones.

Relaxing these requirements would help meet the intent of HALA and also reduce the MHA burden. It would let homebuilders actually use the upzone MHA grants them.

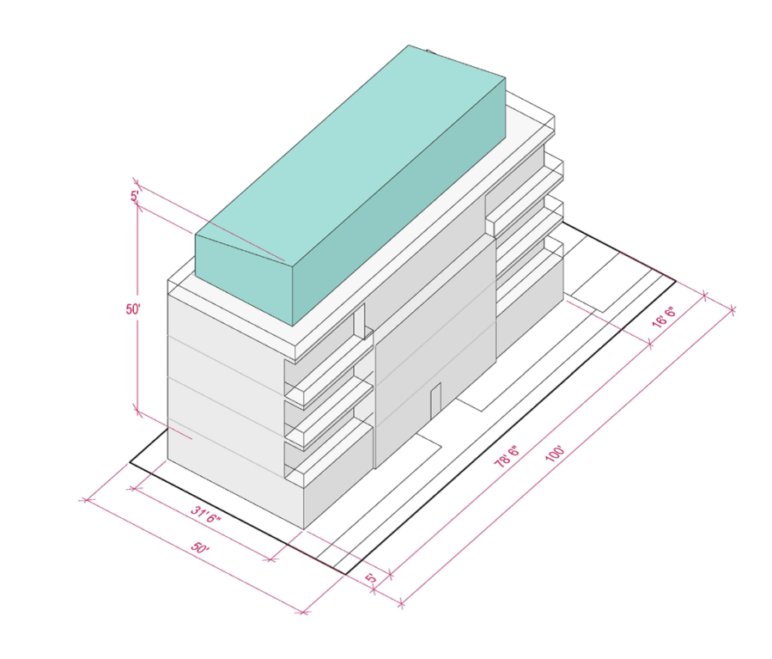

City of Seattle diagram of the LR3 small apartment prototype illustrating 12-foot setbacks on the 5th floor (shown in turquoise) as would be required under the proposed MHA upzone.

The MHA upzones for both LR2 and LR3 add a new requirement for 12-foot setbacks on the top floor (see diagram above). I assumed that these setbacks add a 1 percent premium to the building’s total construction cost, which may be an underestimate of the added cost. For the larger LR3 prototype, that’s an extra $93,000—about 6 percent of the ROI—out of the homebuilder’s pocket. For the larger LR3 prototype, increasing the FAR to 2.5 and eliminating the setback requirement would bring the ROI under MHA up to 14.6 percent. In practice, MHA’s setback requirement prioritizes some people’s opinions about how a building might look over other people’s need for a place to live.

On the other hand, Seattle’s low-rise zones were designed for relatively small-scale housing. If officials opt not to upsize the buildings further, they could instead balance MHA by reducing the affordability requirements. How much reduction would be needed? For the larger LR3 prototype, lowering the in-lieu fee from the proposed $13.25 to $3 achieves an ROI that matches the existing zoning baseline ROI of 15 percent. For the LR2 prototype, a reduction of the in-lieu fee to $8 would do the same.

Keeping the affordability promise

Done right, MHA can deliver affordability two ways: by helping Seattle neighborhoods add enough homes of all kinds to keep prices down overall and by leveraging new building to invest in subsidized homes across the city . Done wrong, it will hamper both. Discouragingly, the current draft low-rise MHA proposal is more likely to hamper than deliver. City leaders can avoid this damaging misstep by enlarging the proposed upzones, or dialing back the proposed mandates and fees, or a bit of both.

Unfortunately, a pattern is emerging among the MHA upzones I have so far analyzed: they all lean by varying degrees toward diminished homebuilding and the lose-lose outcome of fewer new affordable homes and fewer new market-rate homes. If the city hopes to implement an MHA program that doesn’t risk doing more harm than good for affordability overall, policymakers must do the math and bring MHA into balance.

The table below shows the FAR limits for the four building types allowed in Seattle’s low-rise zones, under existing zoning and under the currently proposed MHA upzones. The change in FAR—the most fundamental determinant of the value of the upzone—varies substantially depending on both the zone and building type. Note that to encourage small apartments the proposed LR1 upzone removes the existing unit density limit and exempts partially below-grade units from FAR, although it also adds a requirement for family-sized units. The proposed LR1 upzone was not analyzed in this article because it would involve a major change in building type from a for-sale to a rental product, complicating the value comparison. Given the generous FAR boost of 30 percent, the proposed LR1 upzone would likely result in a preserved or even improved return on investment compared to existing zoning.

Pro forma input assumptions were taken from the city’sMHA feasibility study and are summarized in the tables below. For simplicity parking was not included in the prototypes. Including parking would not significantly alter the change in ROI before and after MHA, and in higher density areas of the city, projects such as these with zero parking are not uncommon. The assumption of a 1 percent cost premium for the loss of efficiency and added expense of the upper level setback is likely conservative. For a cost premium of 2 percent on the large LR3 prototype, the loss of ROI caused by MHA would increase from 25 percent to 30 percent.

Pro forma data are given in the tables below, including the three prototypes discussed in the article, along with results for the larger LR3 prototype in both low and high market-strength areas to illustrate qualitatively similar results. Note that the city’s larger LR3 prototype includes 7000 square feet of partially underground units that don’t count toward FAR but do count for calculating the MHA requirements.

Weekend Reading 3/10/17

Kelsey

Over dinner the other night, one of my friends proclaimed, “I’m currently at war with my cell phone.” I immediately laughed this off as another one of his hyperboles and took the light rail home, watching nearly all my fellow passengers frown into the blue-light of their screens. Soon after, I ran across this PBS interview with Tristan Harris, a former Google “product philosopher.” Tristan’s main point is that product developers are not too concerned with whether or not their tools impact your life in a positive way–instead, it’s all about maximizing the amount of time you spend on your device. Here is a particularly haunting quote from the aforementioned interview: “Never before in history have 50 mostly male, 20-35 year old designers in California, working at three tech companies, influenced how a billion people spend their time.”

This wasn’t an earth-shattering revelation for me, but nevertheless I decided to join my friend in the war against cell phones and have now started to incorporate the Amazing Hour into my daily schedule. The result? I’m sleeping better, waking up earlier, and I’m happier.

Vox reported this week that “advanced energy” (business sectors that reduce energy consumption and fossil fuel emissions) brought in $1.4 trillion in global revenue last year. That’s twice the global revenue of the airline industry. In the United States, the advanced energy industry brought in as much revenue as the pharmaceutical industry in 2016—$200 billion. According to a report by trade association Advanced Energy Economy, the clean energy industry is growing twice as fast as the world economy (7 percent vs 3.1 percent). Though not all the categories in the report are things I would label “clean energy,” Vox’s summary of the report is worth a look.

On Thursday, small business owners in Greenwood marked the one year anniversary of the methane gas pipeline explosion that destroyed several of their businesses and severely damaged others. I attended the press conference and was disheartened to learn that many Greenwood business owners are still struggling to get back on their feet and be made whole for their losses. Puget Sound Energy is facing a $3.2 million fine for improperly abandoning the gas pipeline that caused the blast. On the anniversary of the explosion, they canvassed the Greenwood commercial center to educate the public about natural gas safety. Wouldn’t a more relevant step on their part be figuring out where their other abandoned pipelines are (seriously, they say they don’t know) and fixing them before this happens again?

Alan

I’ve noticed two Cascadians in the new US Cabinet. The Seattle Times profiled Defense Secretary Doug Jim Mattis of Washington’s Tri-Cities, and the New York Times did a portrait of Interior Secretary Ryan Zinke, who is from Whitefish, Montana. (Sightline wrote about him too.) Are there others? Let us know in comments.

A thoughtful reflection on the meaning of sanctuary—the parallels between inclusion and exclusion in immigration policy and land-use policy––from a local officials in a suburb of Boston.

I’m continuing my reading marathon on race and incarceration in the United States. This week, I read Brown University economist Glenn Loury’s 2002 book The Anatomy of Racial Inequality. The book brings together economics, game theory, moral and political philosophy to factor out phenomena like racial discrimination and prejudice, which it argues are overbroad terms, into a nuanced and rigorous anatomy of concepts. With these concepts, it becomes much easier to differentiate and discuss both race relations and discourse about race relations. Reading it took me back to my undergraduate days reading philosophers such as John Rawls, sometimes in a good way and sometimes in a strenuously academic way. But I feel better equipped for having read it. Here’s one of the concluding paragraphs to give a taste:

The unfair treatment of persons based on race in formal economic transactions is no longer the most significant barrier to the full participation of blacks in American life. More important is the fact that too many African Americans cannot gain access on anything approaching equal terms to social resources that are essential for human flourishing, but that are made available to individuals primarily through informal, culturally mediated, race-influenced social intercourse. It follows that achieving racial justice at this point in American history requires more than reforming procedures so as to ensure fair treatment for blacks in the economic and bureaucratic undertakings of private and state actors.

And this New York Times columnby Eduardo Porter does a good job of exposing the class resentments that make anti-poverty social programs hard to sustain. A better political approach than means-tested social programs is universal social insurance programs and other universal benefits. Social Security and Medicare are sacrosanct in the United States, while the range of welfare programs keep getting cut. Social Security has cut senior poverty more than poverty among any other age cohort in the United States. Dividends from the Alaska Permanent Fund carry no stigma and enjoy widespread popular support. Universal insurance programs and benefits—perhaps someday including guaranteed basic income—have political staying power that the more economically cost-effective means-tested programs will never have. They also tend to be much more generous and therefore better at reducing poverty and dampening inequality.

Kristin

New America’s Lee Drutman makes the case that a too-strong presidency and a too-weak congress (paralyzed by partisanship) are ruining America. Maine voters are pointing the way to a solution by approving ranked-choice voting, and we could also try proportional representation.

An oldie-but-goodie: Civil rights hero Lani Guinier makes the case that multi-winner districts with cumulative voting are a better civil rights solution than race-conscious districting.

If your language has a word for a specific emotion, does that make it easier for people in the culture to feel that way? Couldn’t we all do with feeling a bit more mbuki-mvuki (Bantu) – the irresistible urge to “shuck off your clothes as you dance”? Or Shinrin-yoku (Japanese) – the relaxation gained from bathing in the forest. And certainly we could use more Dadirri (Australian aboriginal) – a deep, spiritual act of reflective and respectful listening.

Eric

Check out this Yale University map of climate change public opinion in the US with data down to the county level. It’s fascinating. And also perplexing, as when one finds counties where substantially more people believe that global warming is happening than who believe that scientists believe global warming is happening. On balance, I can’t decide whether the portrayal is encouraging or disheartening.

(Side-note: I can’t stand it when displays of information are improperly color coded like this one it. The low end of the range is shaded dark blue while the high end of the range is shaded purple, which makes the two extremes look similar to one another and dissimilar from the muted tones of the middle ground. That’s a graphic design party foul.)

Yes! Magazine, devoted its Spring 2017 to science, explaining why scientists need to speak truth to power, and describing how “citizen science,” has advanced knowledge and aided communities at the same time. On a similar topic, Grist reported that a key organizer in the March for Science is a professional climate researcher at the University of Washington. The March is now planned for Earth Day, April 22. You can find the project’s mission statement and a march near you on the website.

John Abbotts is a former Sightline research consultant who occasionally submits material for Weekend Reading and other posts.

A Victory for Coal Mine Cleanup

The tsunami of bankruptcies that overwhelmed the US coal industry over the past two years has largely subsided—but it left an unprecedented path of financial wreckage in its wake, wiping out shareholders, decimating balance sheets, and stranding billions of dollars in loans that will never be repaid.

There’s been an unexpected upside to this financial chaos, however: an obscure federal subsidy to the coal industry has been all but eliminated. The subsidy, called “self-bonding,” was essentially a loophole in federal law that allowed “financially healthy” coal companies to avoid setting aside money to clean up their mines. (Here’s our simple “explainer” on the topic.) Yet as the massive wave of coal industry bankruptcies amply demonstrated, coal companies that seemed healthy on paper could quickly descend into insolvency, potentially leaving no resources to pay to clean up their played-out mines. As state and federal regulators realized that they faced a looming mine cleanup crisis they began to rein in self-bonding—and some industry executives acted to replace their self-bonds on their own terms before regulators beat them to it.

Vast swaths of mined land that were once protected by little more than a wink and a promise will be covered by more financially robust cleanup assurances.

On Monday Peabody Energy became the latest company to announce that it would no longer take advantage of the self-bonding loophole, and would put firmer cleanup guarantees in place. Cloud Peak Energy, which didn’t go through bankruptcy, voluntarily exited self-bonding earlier this year, and peers Arch Coal and Alpha Natural Resources (now Contura Energy) replaced their self-bonds as they emerged from bankruptcy.

This means that all ofthe top coal companies in Wyoming’s Powder River Basin have either stopped, or committed to stop, the practice of self-bonding. Self-bonds remain in place at one of the basin’s smaller mines, but vast swaths of mined land that were once protected by little more than a wink and a promise will be covered by more financially robust cleanup assurances.

Self-bonding always suffered from three fundamental flaws. First, the self-bonding loophole shifted risks from coal companies onto the public—potentially forcing cash-strapped states to pay for mine cleanup, or leaving local communities and downstream neighbors to deal with the consequences of living near an unreclaimed mine. Second, the loophole amounted to a direct subsidy to the coal industry, allowing coal companies to avoid paying for mine cleanup insurance or setting aside cash or other resources to guarantee mine reclamation. Third, the rules for deciding whether a company is “healthy” were completely broken, and allowed many companies to remain eligible to self-bond right up to the brink of bankruptcy. Self-bonding has led to a looming mess in West Virginia: one coal company exited bankruptcy without enough money to replace its self-bonds. Its West Virginia mines are still operating with no guarantee that there will be enough money to reclaim the land after the mines are closed.

For several years I’ve been arguing that the right way to deal with self-bonding is to eliminate it completely. Recent history has proven beyond a doubt that it’s a risky practice rife with abuse. Barring that, federal regulators could rewrite the rules, making sure that companies with even a hint of financial weakness should be required to put up stronger cleanup assurances. Of course, the first solution requires the US Congress to act, while the second requires the administration to do so. Neither seems likely at present.

In the meantime, I count Peabody’s withdrawal from self-bonding as good news. If the company thrives after emerging from bankruptcy, it will prove that coal companies don’t actually need the subsidy at all. But if the company’s finances falter, it will demonstrate that self-bonding was always a risky choice for a high-risk industry that’s as likely to go bust as it is to boom.

Editor’s note: The report below is an updated version of the original report published in March 2017. Since this report was first published, four BC liquefied natural gas projects have been cancelled. Sixteen LNG proposals are still standing—but most of them are standing still.

Over the past few years, Oregon and Washington fended off several proposals to build enormous fracked fuel and petrochemical terminals on their respective coasts. But just to the north, British Columbia’s political leaders took the opposite tack, sending out a siren song to attract liquefied natural gas (LNG) investors to the province’s western shores.

The invitation lured would-be LNG exporters with the promise of fossil-fuel-friendly policies and cheap fracked gas from fossil fuel basins in northeast BC. Oil and gas companies the world over answered the call, proposing nearly two dozen LNG export facilities designed to ship the liquefied fossil fuel to Asia.

Global LNG prices collapsed shortly after the LNG “gold rush” began, dashing the hopes for profitable BC LNG exports. Some proposals have already closed up shop, but sixteen remain. The projects are clustered in four locations: the Salish Sea, Kitimat, Prince Rupert, and Kitsault. Most of the projects would require new pipelines to move gas from the distant Western Canadian Sedimentary Basin in Northeastern BC, raising concerns that they would undermine the interests of numerous BC First Nations. Some of the projects have also run into public opposition over concerns that they would increase emissions and tanker traffic, and harm critical salmon habitat.

This revised Sightline report, Mapping BC’s LNG Proposals, details the sixteen active BC LNG proposals and offers an overview of each project’s finances, location, export plans, and proposed pipeline infrastructure.

Liquefied Natural Gas: Coming to a Rail Line Near You?

Already besieged by explosive oil trains and polluting coal trains, rail-line communities in the Pacific Northwest may soon face a new vexation: mile-long trains hauling liquefied natural gas (LNG). It’s thanks to a little-known experiment taking place in Alaska, under test conditions that bear little resemblance to realities in Cascadia.

The first LNG-by-rail shipment

For safety reasons, the Federal Railroad Administration (FRA) does not allow railroads in the US to transport LNG by rail. Or rather, it did not allow this until October 2015, when, with virtually no public knowledge about the development, FRA granted a two-year permit to Alaska Railroad, suddenly making it the very first rail corporation in the US to carry the volatile fuel.

Alaska Rail hauled its first LNG cargo in September 2016 as both an LNG tank car demonstration and a cost experiment. It was a move watched eagerly by railroads in the lower 48—including Union Pacific and BNSF, the two dominant rail corporations in Oregon and Washington, which have been seeking authorization to transport LNG by rail from FRA for years. Railroads looking to offset recent losses in coal and oil haulage are looking to LNG, but the challenge is the same one that accompanies all fossil fuel by rail transportation: how to protect public safety.

LNG can erupt into catastrophic explosions, with blast zones larger and more severe than the conflagrations from oil trains.

This opening for LNG-by-rail raises the specter of ever more hazardous rail cargos traveling through Northwest cities and towns if federal regulators and the fossil fuel industry treat Alaska’s experiment with LNG-by-rail as a first step toward approval throughout the US, which is exactly what rail corporations are lobbying FRA to do. But Alaska’s fossil fuel energy requirements and its relatively small and dispersed population are quite different from those of the Lower 48, making it a poor case study for justifying country-wide shipments. And the stakes are high: in the wrong conditions, LNG can erupt into catastrophic explosions, with blast zones larger and more severe than the conflagrations from oil trains.

The causes behind LNG-by-rail development

Interest in LNG-by-rail is a direct consequence of the US boom in fracking that unleashed huge volumes of low-cost natural gas into the market. This, in turn, began underpricing coal for electricity production, thereby driving down coal shipments. Making matters worse for rail corporations, oil-by-rail shipments also decreased in the last several years, primarily due to a downturn in the market for Bakken shale oil. Railroads hope to make up losses from declining oil and coal transportation by hauling new cargos like LNG, which they believe has the potential to generate significant revenues—if only it were legal.

Even without permission to actually haul it, railroads have already been preparing for the day when LNG-by-rail is legal. BNSF, the dominant railroad in the Northwest, has been testing LNG tank cars since at least 2014. By early 2015, BNSF, Union Pacific, Alaska Railroad, and Florida East Coast Railway had all applied for permits to haul the fuel. Even before the Federal Railroad Administration gave Alaska Rail its two-year LNG-by-rail permit in late 2015, natural gas producers had approached tank car manufacturers about developing tank cars suitable for the task.

Why is Alaska the testing ground?

Alaska’s story is peculiar. Although the state is a major producer of coal, oil, and gas, heating fuel and electricity prices in the interior of Alaska are among the highest in the nation. In fact, many residents still use wood-burning stoves and stove oil for heat, which produce high levels of unhealthy particulate matter pollution during the winter. The state’s Interior Energy Project has prioritized LNG as the solution to both energy costs and winter air pollution, particularly for Fairbanks, the largest city in the Alaska interior. Only about 1,000 of Fairbanks’ 32,500 residents and businesses currently use natural gas, but shipping LNG in bulk by rail could theoretically lower the cost of the fuel, making it more attractive to customers.

Rail shipments of LNG would also assist the struggling state-owned Alaska Rail, which has seen substantial losses. Net income for Alaska Rail fell from $14 million in 2013 to $11 million in 2015, and was expected to fall again to $9.3 million in 2016. The rail company’s 2015 annual report attributes the drop in revenue to weakening global coal markets and reduced oil shipments. In January 2017, Alaska Railroad president Bill O’Leary said the railroad is now “anticipating net earnings in the $4-4.5 million range.” LNG-by-rail shipments could help make up some of that revenue shortfall.

Alaska also has another business interest in increasing natural gas consumption. The state purchased the Titan Alaska LNG plant and gas utility provider Fairbanks Natural Gas in 2015. Since there are no pipelines connecting the two, Titan Alaska currently delivers natural gas hundreds of miles north to the Fairbanks utility using LNG tanker trucks. But rail shipments could reduce costs, since one rail car replaces two standard trucks on the road.

Some Alaska citizens and environmental organizations have criticized Alaska Rail and the FRA for using residents as “guinea pigs for the LNG industry,” noting that the agency avoided public input on the LNG-by-rail experiment by failing to disclose the approval process. One environmental organization is suing the railroad administration for information on the risk factors it considered before approving LNG-by-rail in Alaska. The case could ultimately inform the amount of input that Pacific Northwest residents would have on the approval of LNG-by-rail in their own communities.

What’s good for Alaska is not good for the rest of the US

Alaska Railroad says “an optimistic, long-term goal for the project” would be to use LNG-by-rail to supply natural gas to rural Alaska, much as in Japan, which rail companies point to as model. Japan ships LNG by rail in areas where transport by pipeline is not economically feasible, and the cost of truck transport limits the fuel’s delivery range.

Yet even temporary approval in Alaska opens the door for longer-term LNG haulage by railroads in the Lower 48, where the impacts would be much different. Shipping LNG by rail would raise the same concerns as fatally combustible oil trains, but with a fuel that has more numerous and much more complex hazards. In Alaska, most of the LNG rail routes keep the dangerous cargo far from communities and roadways, which would not be true in the continental US. At-grade crossings, where rail traffic interacts with pedestrian and vehicle traffic, are particularly dangerous. These are a comparatively small issue for Alaska Rail—the entire 470-mile route from Seward to Fairbanks has only about a hundred at-grade crossings—but they are much more common in the the Lower 48: BNSF alone has 25,800 at-grade crossings on its rail network.

Another key difference between Alaska and other states is that state ownership of the rail line makes it easier to give notice of fossil fuel shipments to local emergency responders. In the Lower 48, though, the major railroads are corporate entities, and for the most part they are not required to give firefighters any notice of hazardous materials being shipped.

Implications for Cascadia

Federal regulators should not treat the Alaska Railroad experiment as a reason to greenlight LNG-by-rail in other states.

BNSF and Union Pacific have a near-monopoly on rail haulage in the Northwest, and both have applied for permission to ship LNG by rail. Eager to replace sharply declining oil-by-rail cargoes with other products, railroads are looking to LNG in hopes it will yield revenues as coal and oil once did. But rather than deliver natural gas to Northwest residents, the vast majority of whom are already served by gas pipelines, LNG-by-rail through Cascadia would most likely support exports or other large fossil fuel expansion proposals—all at the expense of increased risks for communities along the rail lines.

Railroads are federally regulated, so state and local governments have very little say over what rail corporations push through their towns. It’s a risky proposition for regions like the Northwest that could potentially see new and extremely hazardous rail cargoes passing through the heart of the region’s biggest cities. Federal regulators should not treat the Alaska Railroad experiment as a reason to greenlight LNG-by-rail in other states. To the contrary, the Alaska experiment should remain a limited decision subject to more extensive review and a robust opportunity for public input.

Cloud Peak Retreats from Coal Exports

In another sign of the collapsing prospects for West Coast coal exports, Cloud Peak Energy—one of the largest coal producers in the American West and the best positioned coal exporter in the vast Powder River Basin—recently announced that it had extricated itself from long-term contracts to move coal into Pacific Rim markets. It was a costly retrenchment: the company gave up nearly $10 million that was held in escrow accounts and still committed to make at least $51 million in payments to rail and port companies over the next two years.

But despite the costs, industry analysts generally cheered the move. As well they should have: under its prior contracts, Cloud Peak had committed to pay $475 million in port and rail fees between 2019 and 2024, even if the company didn’t ship a single ton of coal to Asia.

Canceling these export contracts represented a remarkable about-face for the company. As recently as mid-2013, Cloud Peak executives practically bubbled with optimism about the company’s bright prospects for exporting coal into burgeoning Pacific Rim coal markets, boasting to investors that they had made Asian exports the centerpiece of their corporate growth strategy. The company ultimately committed hundreds of millions of dollars to an ambitious, multi-pronged export strategy, which included:

Long-term contracts with rail company BNSF to ship coal from its Powder River Basin mines to the coastal coal terminals;

Long-term contracts with the Westshore export terminal in southwestern British Columbia to load coal onto ships bound for Asia;

A 49 percent stake in the proposed Gateway Pacific coal export terminal outside Bellingham, Washington;

Port access rights at the proposed Millennium Bulk Terminal in Longview, Washington;

Development of two new export-oriented coal mines in the Powder River basin.

That strategy has almost completely unraveled. China’s coal demand, which once looked limitless, has fallen for three consecutive years, driven by government policies designed to rein in pollution and modernize the nation’s economy. As Chinese coal demand waned, prices fell—submerging Cloud Peak’s export business in a sea of red ink. By late 2015 Cloud Peak’s export losses were mounting so rapidly that the company decided it would actually be cheaper to pay shipping partners notto ship coal—a move that forced the company’s accountants to completely write off the value of its export contracts and port rights.

The coal export pipe dream continues to fade away, leaving a bad hangover on coal industry’s balance sheets and a lingering bad taste in the mouths of coal investors and executives alike.

At the same time, politics also took its toll on Cloud Peak’s export ambitions. Last May the US Army Corps of Engineers halted the Gateway Pacific terminal, citing concerns over Native American treaty rights; the company backing the terminal gave up its fight for the project last month. And last December the state of Washington denied a critical sublease to the Millennium terminal, arguing that the project’s backer failed to provide information about its business plan—information that may well have shown that there wasn’t a viable business plan, given the dismal state of international markets, plus the fact that the terminal’s sole remaining partner pulled out of the project after declaring bankruptcy. (And as a side note, the terms of Cloud Peak’s new contracts undermine Millennium’s prospects still further: Cloud Peak gave the Westshore terminal the right of first refusal for coal export shipments through 2024, which would deny Millennium a key potential customer.)

Cloud Peak’s bad luck streak eased a bit last fall, after government-mandated cutbacks in Chinese coal production breathed some life into torpid coal markets. As seaborne coal prices ticked upwards Cloud Peak managed to sign contracts to ship more than a million tons of coal to Korea. It was a far cry from the multi-million-ton export business the company had previously banked on—but much better than paying steep fees to export nothing at all, as the company had done for most of the previous year.

Still, it’s clear that the years of red ink, political losses, and painful asset write-downs have dashed Cloud Peak’s confidence in its export strategy. In his last investor call, the company’s CEO conceded that international competitors would always have a leg up on Cloud Peak in Asian markets:

I think realistically, we’re never going to be at the low—the bottom of the cost curve internationally because of just the distance we are from the coast and compared to Indonesia and to the customers compared to Indonesia. So, we need to recognize that and position ourselves accordingly.

And even though international coal prices are much higher now than they were a year ago, the company acknowledged that Pacific Rim coal futures prices are still too low for the company to lock in long-term profits. Moreover, Cloud Peak’s executive team seems to recognize that Pacific Rim coal prices are driven almost entirely by the whims of Chinese policymakers—and that counting on Beijing to be nice to the US coal industry is a sucker’s game. These developments help explain why Cloud Peak has removed Asian exports from the center of its corporate strategy, even as the company has begun to search for new domestic customers to replace its lost export opportunities.

I have to think that Cloud Peak’s executives once imagined themselves as rising stars in the international coal game. But they’ve finally admitted to themselves that they are bench players at best: shipping a bit of coal when prices are high, but otherwise sitting on the sidelines.

The same is true for the rest of the coal industry in the US West. Robust, sustainable Asian coal markets were never a realistic hope for US coal exporters: the transportation costs were too high, the competition too fierce, and the demand too unstable. So the coal industry’s PR flacks may continue to spin tales about endless riches in the Asian coal market, the financials are telling a much more sobering story: that the coal export pipe dream continues to fade away, leaving a bad hangover on the coal industry’s balance sheets and a lingering bad taste in the mouths of coal investors and executives alike.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognizing you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

3rd Party Cookies

This website uses Google Analytics to collect anonymous information such as the number of visitors to the site, and the most popular pages.

Keeping this cookie enabled helps us to improve our website.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Additional Cookies

This website uses social media to collect anonymous information such as which platform are our users coming from.

Keeping this cookie enabled helps us better reach our audiences.

Please enable Strictly Necessary Cookies first so that we can save your preferences!